Füllen Sie das untenstehende Formular aus, um Zugang zu unserem zusammenfassenden Dokument zu erhalten, das alle wichtigen Informationen enthält.

REGELUNG Zentrum

EU-Taxonomie

Bei der EU-Taxonomie handelt es sich um eine Klassifizierung, die Kriterien festlegt, anhand derer bestimmt werden kann, ob eine Wirtschaftsaktivität wesentlich zu den sechs in der Verordnung festgelegten Umweltzielen beiträgt. Sie ist ein Instrument, das Unternehmen und Investor:innen dabei hilft, nachhaltige Investitionsentscheidungen zu treffen. Die Angaben zur EU-Taxonomie müssen im Rahmen der Non-Financial Reporting Directive (NFRD)/Corporate Sustainability Reporting Directive (CSRD)- und der Sustainable Finance Disclosure Regulation (SFDR)-Reportingpflichten gemacht werden.

Bei der EU-Taxonomie handelt es sich um eine Klassifizierung, die Kriterien festlegt, anhand derer bestimmt werden kann, ob eine Wirtschaftsaktivität wesentlich zu den sechs in der Verordnung festgelegten Umweltzielen beiträgt. Sie ist ein Instrument, das Unternehmen und Investor:innen dabei hilft, nachhaltige Investitionsentscheidungen zu treffen. Die Angaben zur EU-Taxonomie müssen im Rahmen der Non-Financial Reporting Directive (NFRD)/Corporate Sustainability Reporting Directive (CSRD)- und der Sustainable Finance Disclosure Regulation (SFDR)-Reportingpflichten gemacht werden.

Was ist die EU-Taxonomie?

Die EU-Taxonomie ist eine Klassifizierung, die Kriterien festlegt, anhand derer bestimmt werden kann, ob eine Wirtschaftstätigkeit wesentlich zu den sechs in der Verordnung festgelegten Umweltzielen beiträgt:

◦ Klimaschutzmaßnahmen

◦ Anpassung an den Klimawandel

◦ Nachhaltige Nutzung und Schutz von Wasser- und Meeresressourcen

◦ Übergang zu einer kreislauforientierten Wirtschaft, einschließlich Abfallvermeidung und Recycling

◦ Vermeidung und Kontrolle von Umweltverschmutzung

◦ Schutz gesunder Ökosysteme.

Die EU-Taxonomie ist ein Werkzeug, um Unternehmen und Investoren bei der Entscheidung über nachhaltige Investitionen zu unterstützen.

Die EU-Taxonomie ist Teil des EU-Pakets für nachhaltige Finanzen, welches darauf abzielt , den Geldfluss in Richtung nachhaltiger Aktivitäten in der Europäischen Union zu verbessern.

Diese Einheiten müssen über den Grad der Taxonomieausrichtung ihres Finanzprodukts im Rahmen ihrer produktbezogenen Offenlegungen nach der EU-SFDR (vorkontraktuelle und periodische Offenlegungen) berichten.

Nicht-EU-Unternehmen im Anwendungsbereich der NFRD/CSRD

Unternehmen, die Wertpapiere an einem von der EU regulierten Markt notiert haben

Nicht-EU-Unternehmen (einschließlich EU-Tochtergesellschaften eines britischen Mutterkonzerns) mit einem Jahresumsatz in der EU von > 150 Millionen € und einer EU-Niederlassung mit einem Nettoeinkommen von > 40 Millionen €

Unternehmen mit mindestens einer EU-Tochtergesellschaft (entweder ein großes EU-Unternehmen oder ein EU-Unternehmen, das an einem von der EU regulierten Markt notiert ist und kein Kleinstunternehmen darstellt), das mindestens zwei der folgenden drei Kriterien erfüllt:

mehr als 250 EU-basierte Mitarbeiter

Bilanz > €20 Millionen

lokaler Umsatz von über 40 Mio. €

Was muss offengelegt werden?

Aufgrund der Komplexität der EU-Taxonomie und da Teile der Methodik noch definiert werden müssen, werden die Offenlegungspflichten für Unternehmen in den nächsten vier Jahren schrittweise eingeführt.

Das endgültige Ziel der Anforderungen ist es,:

Unternehmen, die in den Anwendungsbereich der CSRD/NFRD fallen, müssen den Anteil ihrer "ökologisch nachhaltigen" wirtschaftlichen Aktivitäten (wie durch die EU-Taxonomie definiert) in ihren Einnahmen, Capex und OPEX berichten.

Finanzmarktteilnehmer müssen offenlegen, wie ihre Finanzprodukte im Rahmen der SFDR mit der EU-Taxonomie übereinstimmen.

Wo muss berichtet werden?

Unternehmen, die in den Anwendungsbereich der CSRD/NFRD fallen, müssen ihre Taxonomie-Offenlegung im jährlichen CSRD/NFRD-Bericht melden, welcher zusammen mit dem Unternehmenslagebericht veröffentlicht werden muss.

Die Taxonomie-Offenlegung von Unternehmen im Geltungsbereich der SFDR muss in periodischen Überprüfungen und vorvertraglichen Offenlegungen veröffentlicht werden.

Der aktuelle Stand der Taxonomie-Umsetzung

Zusätzlich zu den CSRD-Berichtspflichten müssen die betroffenen Unternehmen ab Januar 2022 den Prozentsatz ihrer wirtschaftlichen Aktivitäten offenlegen, die für die EU-Taxonomie (für 2022) förderfähig sind.**

Zusätzlich zu den SFDR-Anforderungen müssen Finanzinstitute ab Januar 2022 den Anteil ihrer Gesamtvermögenswerte offenlegen, der auf Taxonomie-nicht-geeignete und Taxonomie-geeignete wirtschaftliche Aktivitäten entfällt.

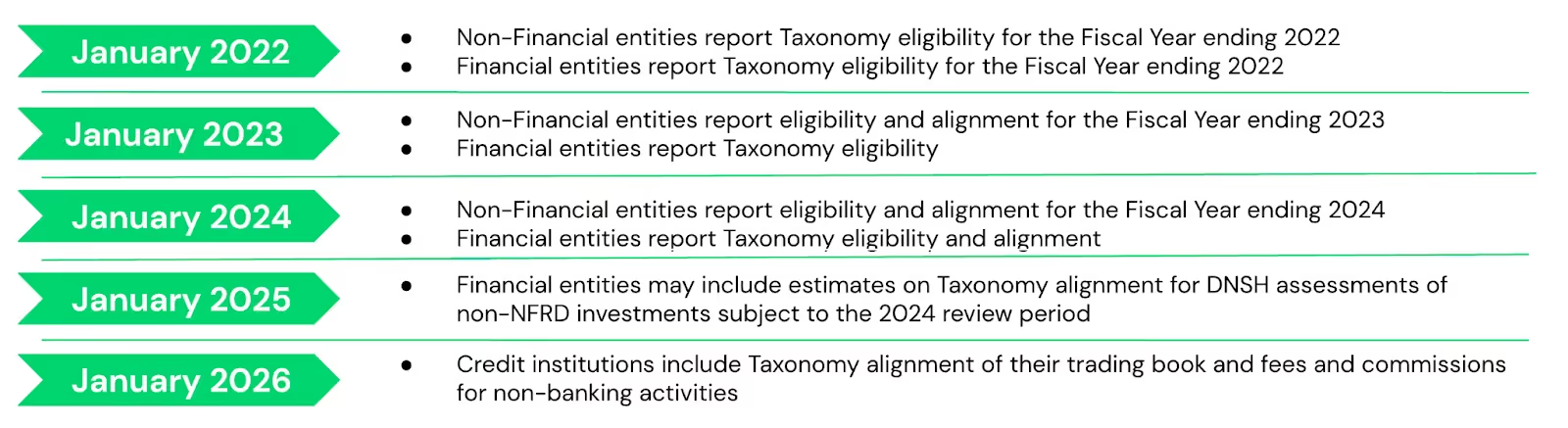

Zeitplan der Offenlegungsanforderungen

Ab 2025 (für das Geschäftsjahr 2024) müssen Unternehmen ihre Taxonomie-Informationen als Teil ihres nichtfinanziellen Berichts gemäß den European Sustainability Reporting Standards (unter der CSRD) offenlegen.

Sie müssen in ihrem CSRD-Bericht den Anteil ihres Umsatzes, der Investitionsausgaben (CapEx) und der Betriebsausgaben (OpEx), der durch ihre wirtschaftlichen Aktivitäten erzielt wird und mit der EU-Taxonomie übereinstimmt, angeben.

Bis dahin müssen nichtfinanzielle Unternehmen im Geltungsbereich der CSRD/NFRD weiterhin ihre Taxonomie-Informationen als Teil ihres nichtfinanziellen Berichts an die CSRD/NFRD offenlegen.

Siehe weitere Details im untenstehenden Diagramm:

Der Zeitplan der Offenlegungspflichten für die EU-Taxonomie Kredit: Plan A

Werden die Offenlegungspflichten extern abgesichert?

Die nichtfinanziellen Erklärungen von Unternehmen im Anwendungsbereich der CSRD/NFRD unterliegen einer Existenzprüfung durch den Abschlussprüfer. Das EU-Recht erfordert keine Überprüfung des Inhalts der Angaben. Die Erklärungen werden geprüft, jetzt, da die CSRD* in Kraft ist.

Die Einhaltung der Offenlegungen von Finanzinstituten, die der SFDR unterliegen, wird von den zuständigen Behörden überwacht.

* Die Richtlinie über die Nachhaltigkeitsberichterstattung von Unternehmen (CSRD) ersetzt die Richtlinie über die nichtfinanzielle Berichterstattung (NFRD). Mit der CSRD unterliegen mehr Unternehmen den Berichtspflichten, die die EU festlegen wird, und die Offenlegungen werden einer externen Prüfung unterzogen. Weitere Informationen finden Sie hier.

** Die Eignung zeigt an, dass ein Unternehmen Geld in einer Tätigkeit verdient, die unter die EU-Taxonomie geprüft werden kann.

Die Uhr tickt! Beginnen Sie noch heute mit der Berichterstattung über Ihre Auswirkungen. Kontaktieren Sie unsere Politikspezialisten, um Lösungen zu entdecken, die auf Ihre Bedürfnisse im Bereich der Nachhaltigkeitsberichterstattung zugeschnitten sind.

Nachhaltigkeit ist ein tiefes und weites Meer, das es zu navigieren gilt. Nutzen Sie mein Wissen und meine Intelligenz, um exponentiell zu lernen und die richtigen Ressourcen zu finden, um Ihre Argumentation zu untermauern.

.webp)