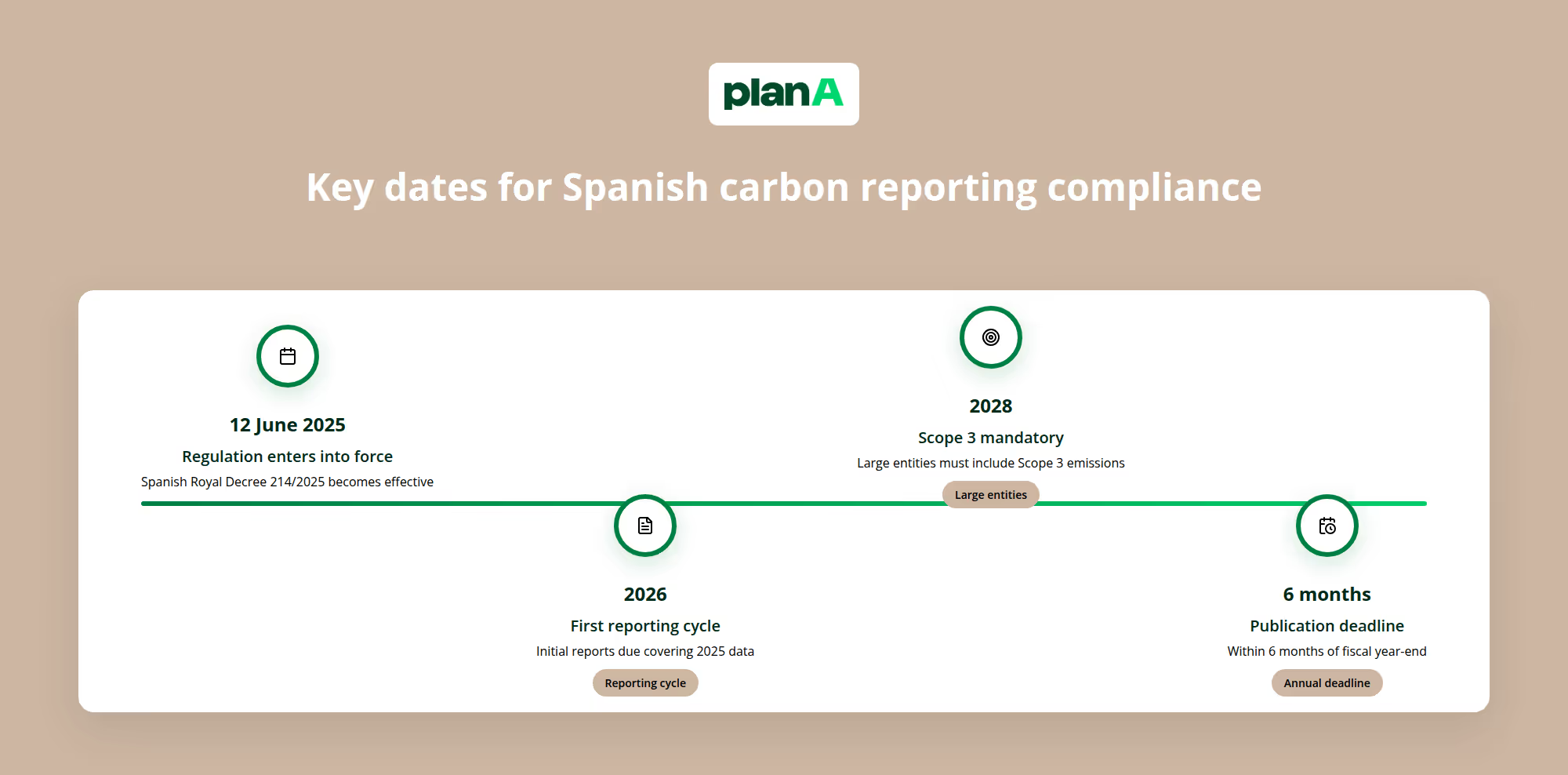

Spanien hat gerade die Anforderungen an die Unternehmerische Nachhaltigkeit erhöht. Das königliche Dekret 214/2025, das am 12. Juni 2025 in Kraft tritt, verwandelt die CO₂-Reporting von einem Nice-to-have in eine gesetzliche Verpflichtung für Tausende von spanischen Unternehmen. Dies ist eine große Veränderung in der Art und Weise, wie spanische Unternehmen an die Dekarbonisierung herangehen. Die verpflichtende Berichterstattung scope 1 und 2 beginnt sofort und scope 3 folgt bis 2028.

Das Dekret setzt zentrale Elemente der Richtlinie zur Berichterstattung über die Unternehmerische Nachhaltigkeit (CSRD) vor Ort um und spannt ein viel größeres Netz als frühere freiwillige Rahmenwerke. Rund 4.000 Organisationen, von großen Privatunternehmen über öffentliche Einrichtungen bis hin zu Veranstaltern, müssen nun umfassende CO2-Fußabdrücke und Fünfjahrespläne zur Reduzierung der Emissionen erstellen. Die Nichteinhaltung hat eine ernste Konsequenz: den Ausschluss von öffentlichen Ausschreibungen - ein Risiko, das sich kein Unternehmen auf dem großen spanischen Markt des öffentlichen Sektors leisten kann.

Zusammenfassung

Das Königliche Dekret 214/2025 ist Spaniens bisher ehrgeizigstes CO₂-Reporting für Unternehmen. Die Verordnung erweitert die Berichtspflicht von einer ausgewählten Gruppe von Unternehmen, die bereits unter das spanische Gesetz 11/2018 fallen, auf alle großen Unternehmen, die bestimmte Schwellenwerte erreichen, öffentliche Einrichtungen und Veranstalter, die Versammlungen mit mehr als 1.500 Teilnehmern organisieren.

Zu den wichtigsten Verpflichtungen gehören:

- Obligatorische Berichterstattung über scope 1 und 2 Emissionen ab 2025

- Scope 3 Emissionen für große Unternehmen ab 2028 erforderlich

- Quantifizierte Fünfjahrespläne zur Reduzierung von Treibhausgas

- Öffentliche Bekanntgabe über das nationale Kohlenstoffregister oder Online-Veröffentlichung

- Jährliche Einhaltung der technischen Spezifikationen von MITECO

Die Verordnung tritt sofort in Kraft. Die ersten Berichte sind im Berichtszyklus 2026 fällig und umfassen die Emissionsdaten für 2025. Unternehmen haben ab dem Ende des Geschäftsjahres sechs Monate Zeit, um ihre CO2-Bilanz und ihre Reduktionspläne zu veröffentlichen.

Wie lautet die Verordnung

Das Königliche Dekret 214/2025 legt Spaniens neuen nationalen Rahmen für CO₂-Reporting fest, der auf bestehenden europäischen Nachhaltigkeitsrichtlinien aufbaut und gleichzeitig spanienspezifische Anforderungen schafft. Das Ministerium für den ökologischen Wandel und die demografische Herausforderung (MITECO) dient als Durchsetzungsbehörde, die die technischen Anforderungen festlegt und die Einhaltung überwacht.

Im Gegensatz zu rein freiwilligen Nachhaltigkeitsinitiativen hat dieses Dekret rechtliches Gewicht. Zwar werden keine konkreten finanziellen Strafen genannt, aber die Nichteinhaltung führt zum Ausschluss von öffentlichen Ausschreibungen - ein erhebliches Geschäftsrisiko, wenn man bedenkt, dass die Ausgaben des öffentlichen Sektors etwa 18 % des spanischen BIP ausmachen.

Rechtsgrundlage und Anwendungsbereich

Das Dekret setzt Teile der CSRD auf nationaler Ebene um und schafft einen umfassenden Rahmen für die CO₂-Bilanzierung , der über die traditionelle Berichterstattung großer Unternehmen hinausgeht. Es verpflichtet die betroffenen Unternehmen, ihre Treibhausgas nach international anerkannten Methoden zu berechnen, quantifizierte Reduktionsziele für mindestens fünf Jahre festzulegen und ihre Fortschritte öffentlich bekannt zu geben.

Die Verordnung schreibt die Verwendung des Treibhausgas vor, das die Übereinstimmung mit globalen Standards gewährleistet und gleichzeitig spanienspezifische Emissionsfaktoren einbezieht. Dieser Ansatz liefert den Unternehmen lokal relevante Daten und gewährleistet gleichzeitig die internationale Vergleichbarkeit - wichtig für multinationale Unternehmen, die grenzüberschreitend tätig sind.

Anforderungen an die Berichtsmethodik

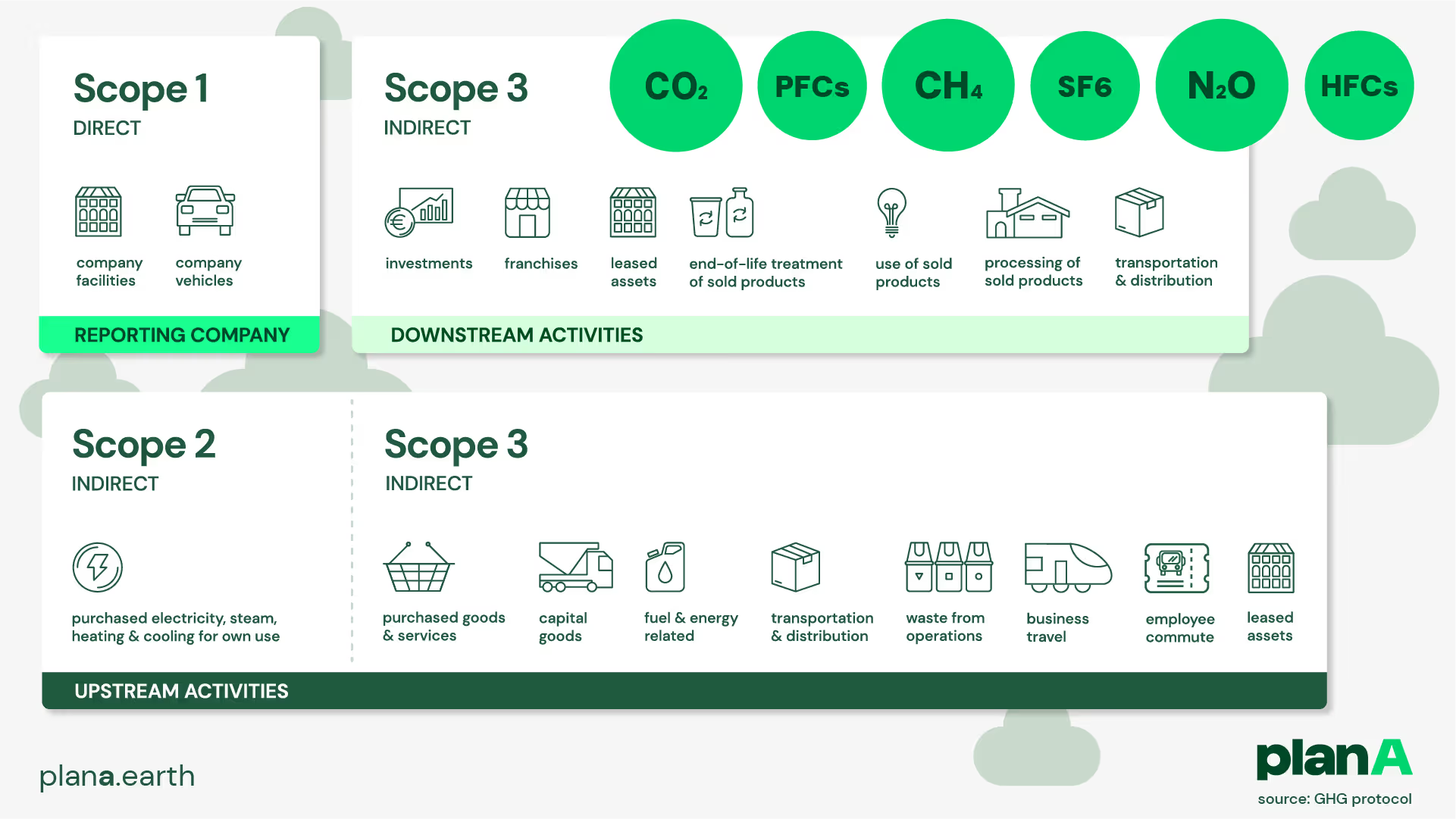

Organisationen müssen ihre Emissionsdaten nach dem Drei-Scope-Rahmen strukturieren: Direkte Emissionen aus eigenen Quellenscope 1), Indirekte Emissionen aus zugekaufter Energiescope 2) und alle anderen Emissionen der Wertschöpfungskettescope 3). Das Dekret verlangt eine detaillierte Aufschlüsselung nach Emissionskategorien, was eine detaillierte Analyse der Kohlenstoff-Hotspots in den verschiedenen Geschäftsbereichen ermöglicht.

Für Unternehmen, die ein Höchstmaß an Genauigkeit anstreben, werden tätigkeitsbasierte Berechnungen mit spezifischen Emissionsfaktoren bevorzugt. Die Verordnung erkennt jedoch die Probleme bei der Datenverfügbarkeit an und erlaubt ausgabenbasierte Berechnungen, wenn primäre Aktivitätsdaten nicht zugänglich sind. Diese Flexibilität gewährleistet eine umfassende Berichterstattung, während die Unternehmen anspruchsvollere Datenerfassungssysteme aufbauen.

Wer ist davon betroffen?

Das Dekret erweitert die spanische CO₂-Reporting erheblich und betrifft etwa 4.000 Unternehmen in drei Hauptkategorien. Dies stellt eine erhebliche Steigerung gegenüber früheren freiwilligen Rahmenregelungen dar und bringt Tausende von Organisationen zum ersten Mal in die Pflicht.

Große Privatunternehmen

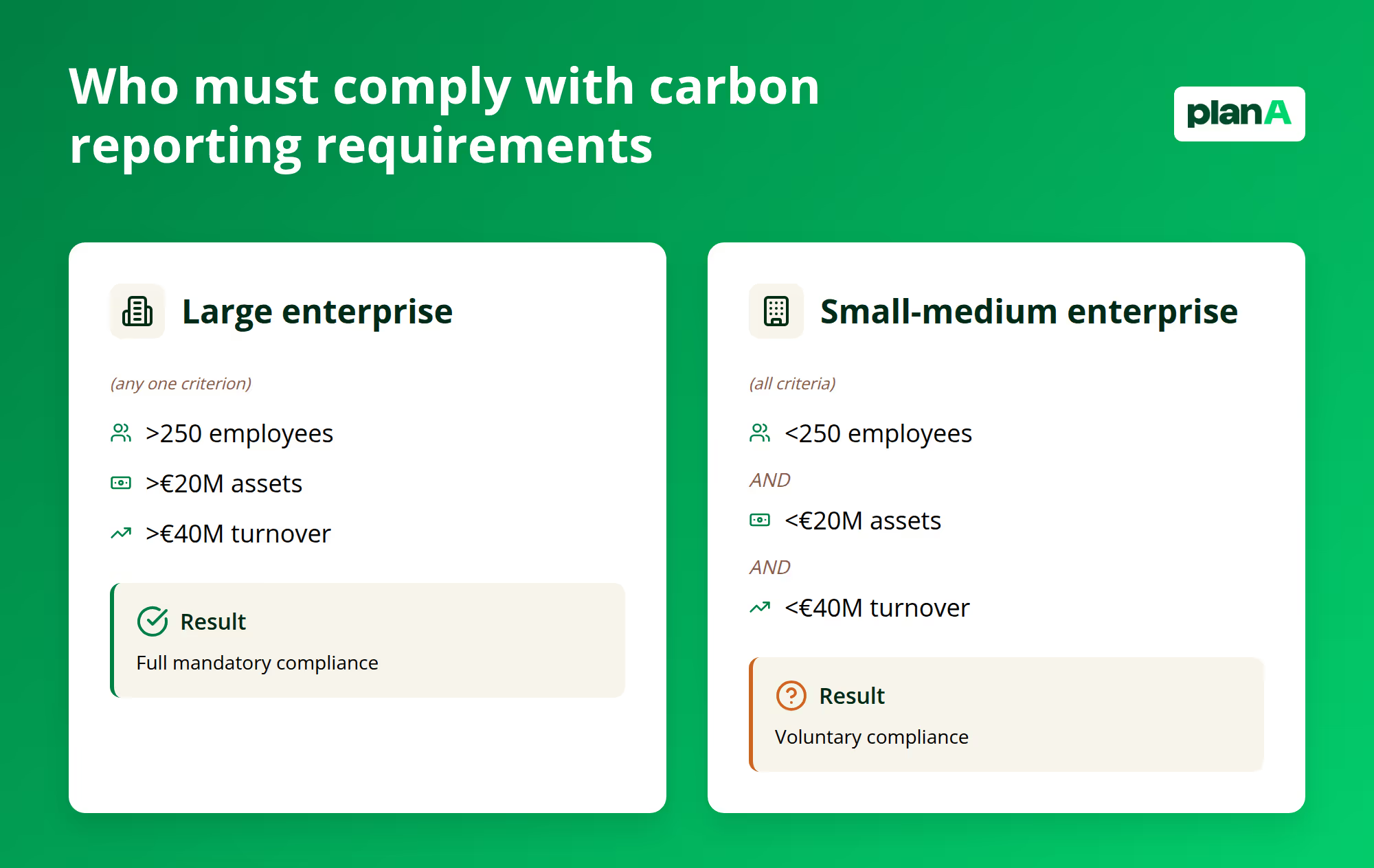

Privatunternehmen müssen die Anforderungen erfüllen, wenn sie in zwei aufeinanderfolgenden Jahren einen der folgenden Schwellenwerte erreichen: mehr als 250 Beschäftigte, mehr als 20 Millionen Euro an Vermögenswerten oder mehr als 40 Millionen Euro an Jahresumsatz. Dies gilt für mittlere bis große Unternehmen aus allen Sektoren, von der verarbeitenden Industrie und dem Einzelhandel bis hin zu professionellen Dienstleistungen und Technologieunternehmen.

Diese Schwellenwerte stimmen mit den bestehenden Anforderungen an die nichtfinanzielle Berichterstattung gemäß dem spanischen Gesetz 11/2018 überein und gewährleisten so die Konsistenz zwischen den verschiedenen Rahmenwerken der Nachhaltigkeitsberichterstattung. Unternehmen, die diesen Anforderungen bereits unterliegen, werden sich auf vertrautem Terrain wiederfinden, obwohl die kohlenstoffspezifischen Verpflichtungen Neuland darstellen und spezielles Fachwissen und Systeme erfordern.

Öffentliche Einrichtungen und Verwaltung

Alle öffentlichen Einrichtungen in Spanien sind zur Einhaltung der Vorschriften verpflichtet, unabhängig von ihrer Größe oder ihrem Budget. Dazu gehören zentrale Regierungsstellen, regionale Verwaltungen, Gemeinden und staatliche Unternehmen, die konsolidierte Abschlüsse erstellen. Öffentliche Einrichtungen müssen mit gutem Beispiel vorangehen und ihr Engagement für die Dekarbonisierung in allen Bereichen der Regierung unter Beweis stellen.

Die Einhaltung der Vorschriften im öffentlichen Sektor erstreckt sich nicht nur auf die internen Abläufe, sondern auch auf die Beschaffungspraktiken. Öffentliche Einrichtungen müssen den CO₂-Reporting von Lieferanten bei der Bewertung von Ausschreibungen berücksichtigen, was sich auf die gesamte spanische Lieferkette auswirkt. Unternehmen, die sich um öffentliche Aufträge bemühen, müssen Kohlenstofftransparenz nachweisen oder riskieren, von lukrativen staatlichen Aufträgen ausgeschlossen zu werden.

Organisatoren der Veranstaltung

Ein einzigartiger Aspekt der spanischen Verordnung betrifft Veranstaltungen mit mehr als 1.500 Teilnehmern. Damit wird der erhebliche CO₂-Fußabdruck großer Versammlungen anerkannt. Veranstaltungsorganisatoren - ob private Unternehmen, öffentliche Einrichtungen oder gemeinnützige Organisationen - müssen die Emissionen aus dem Energieverbrauch des Veranstaltungsortes, den Reisen der Teilnehmer, dem Catering, der Abfallerzeugung und der Unterbringung berechnen und melden.

Diese Anforderung spiegelt das wachsende Bewusstsein für die Umweltauswirkungen von Veranstaltungen wider, von Unternehmenskonferenzen und Messen bis hin zu Kulturfestivals und Sportwettkämpfen. Die CO2-Bilanz von Veranstaltungen zeigt oft erhebliche scope 3 durch die Anreise der Teilnehmer auf, so dass sich durch die Wahl des Veranstaltungsortes, die Förderung des Transports und hybride Veranstaltungsformate Möglichkeiten für eine deutliche Reduzierung ergeben.

Wie Sie berichten

Die spanische CO₂-Reporting folgt einem strukturierten Ansatz, der Konsistenz, Genauigkeit und Vergleichbarkeit für alle berichtenden Unternehmen gewährleisten soll. Das Rahmenwerk bringt internationale Standards und spanienspezifische Anforderungen in Einklang und schafft so ein umfassendes System, das sowohl der Einhaltung von Vorschriften als auch der Entscheidungsfindung dient.

Datenerhebung und Berechnungsmethodik

Eine erfolgreiche Berichterstattung beginnt mit einer systematischen Datenerfassung für alle Emissionsquellen. Organisationen müssen Aktivitätsdaten aus Energierechnungen, Aufzeichnungen über den Kraftstoffverbrauch, Reisekosten, Abfallentsorgungsverträgen und Lieferanteninformationen sammeln. Die Verordnung erlaubt verschiedene Berechnungsansätze, je nach Datenverfügbarkeit und Genauigkeitsanforderungen.

Aktivitätsbasierte Berechnungen bieten die höchste Präzision, indem sie spezifische Verbrauchsdaten mit entsprechenden Emissionsfaktoren multiplizieren. Ein Produktionsunternehmen würde zum Beispiel den Stromverbrauch in Kilowattstunden mit dem spanischen Netzemissionsfaktor multiplizieren, um die scope 2 zu berechnen. Wenn keine Aktivitätsdaten verfügbar sind, werden bei ausgabenbasierten Berechnungen die finanziellen Ausgaben mit sektorspezifischen Emissionsfaktoren multipliziert.

Zu den wichtigsten Datenquellen gehören:

- Energierechnungen und Zählerstände für scope 2

- Aufzeichnungen über den Kraftstoffverbrauch von Firmenfahrzeugen und Einrichtungen

- Reisebuchungssysteme für die Emissionen von Geschäftsreisen

- Abfallentsorgungsverträge und Tonnagenaufzeichnungen

- Nachhaltigkeitsberichte von Lieferanten und Anfragen nach Primärdaten

- Finanzielle Ausgaben für emissionsrelevante Kategorien

Umfangsspezifische Berechnungsanforderungen

Scope 1 umfassen Direkte Emissionen aus Quellen, die der Organisation gehören oder von ihr kontrolliert werden. Für die meisten Unternehmen gehören dazu Erdgasheizungen, Treibstoff für Firmenfahrzeuge und alle Verbrennungsprozesse vor Ort. Produktionsunternehmen müssen auch Prozessemissionen und Flüchtige Emissionen aus Kühlanlagen berücksichtigen.

Scope 2 umfassen Indirekte Emissionen aus gekauftem Strom, Heizung, Kühlung und Dampf. Das sich entwickelnde spanische Energienetz mit einem zunehmenden Anteil an erneuerbaren Energien erfordert eine sorgfältige Abwägung zwischen standortbasierten und marktbasierten Berechnungsmethoden. Unternehmen, die Zertifikate für erneuerbare Energien kaufen, können marktbasierte Methoden verwenden, um ihre Entscheidung für saubere Energie zu reflektieren.

Scope 3 , die ab 2028 für große Unternehmen verpflichtend sind, stellen die größte Komplexität dar. Die Verordnung erfordert eine Bewertung in 15 Kategorien, von gekauften Waren und Dienstleistungen bis hin zur Behandlung von Produkten am Ende ihrer Lebensdauer. Die meisten Organisationen stellen fest, dass die scope 3 70-80% ihres gesamten CO₂-Fußabdruck ausmachen, so dass eine genaue Messung für eine effektive Dekarbonisierung entscheidend ist.

Veröffentlichungs- und Offenlegungspflichten

Organisationen müssen ihre CO2-Bilanzen und Reduktionspläne innerhalb von sechs Monaten nach Ende des Geschäftsjahres über einen von zwei Kanälen veröffentlichen: Spaniens nationales Kohlenstoffregister oder die Online-Veröffentlichung über Unternehmenswebseiten oder Nachhaltigkeitsberichte. Die Veröffentlichung über das nationale Register bietet eine offizielle Anerkennung durch ein CO₂-Reporting .

Die Berichte müssen umfassende, nach Umfang und Kategorie aufgeschlüsselte Emissionsdaten, Erläuterungen zur Methodik, Bewertungen der Datenqualität und Fünfjahrespläne zur Reduzierung mit quantifizierten Zielen enthalten. Das Format der Offenlegung muss mit den technischen Spezifikationen von MITECO übereinstimmen und gleichzeitig für Stakeholder wie Investoren, Kunden und Mitglieder der Gemeinschaft zugänglich sein.

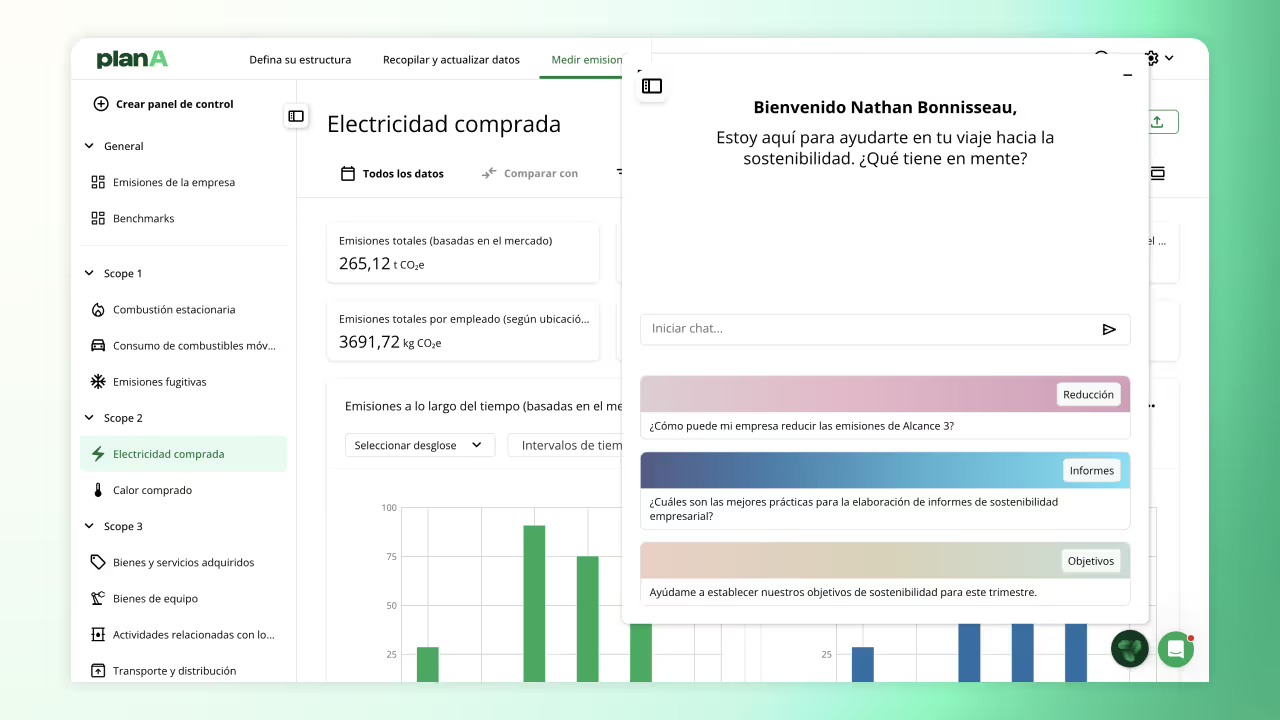

Plattformen wie Plan A rationalisieren diesen Prozess durch die automatische Erstellung von Berichten, die den spanischen gesetzlichen Anforderungen entsprechen und gleichzeitig die für eine effektive Dekarbonisierung erforderlichen detaillierten Einblicke bieten. Die spanienspezifischen Emissionsfaktoren der Plattform gewährleisten eine genaue Berechnung, während integrierte Tools zur Berichterstattung den Veröffentlichungsprozess vereinfachen.

Anforderungen an Verifizierung und Sicherheit

Große Unternehmen und Organisationen, die bestimmte Kriterien erfüllen, müssen ihre CO2-Bilanzen und Reduktionspläne von Dritten überprüfen lassen. Diese Anforderung gewährleistet die Genauigkeit der Daten und stärkt gleichzeitig das Vertrauen der Interessengruppen in die gemeldeten Emissionen. Die Überprüfung umfasst Berechnungsmethoden, Datenquellen, Emissionsfaktoren und die Angemessenheit der Reduktionsziele.

Der Verifizierungsprozess umfasst in der Regel die Überprüfung von Dokumenten, Besuche vor Ort und Tests der wichtigsten Datenquellen. Die Prüfer beurteilen, ob die Organisationen über angemessene Systeme und Kontrollen für die Erfassung von Kohlenstoffdaten verfügen, ob die Berechnungen anerkannten Standards folgen und ob die gemeldeten Emissionen die tatsächliche Leistung angemessen wiedergeben.

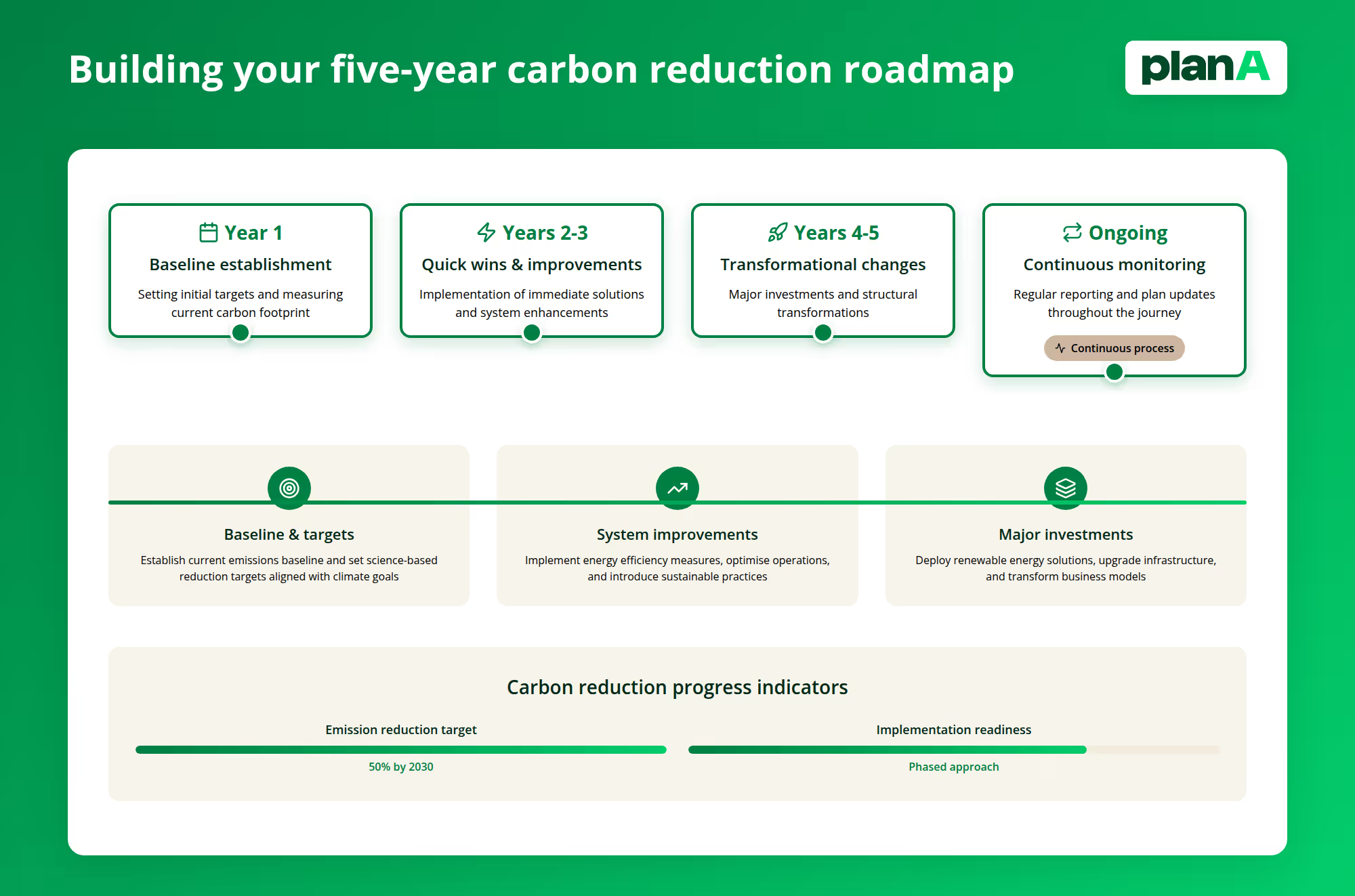

Vorbereitung auf die Verordnung

Die Vorbereitung auf die neuen spanischen CO₂-Reporting erfordert strategische Planung, Systementwicklung und den Aufbau organisatorischer Fähigkeiten. Unternehmen, die frühzeitig damit beginnen, werden die Einhaltung der Vorschriften besser bewältigen können und gleichzeitig wertvolle Erkenntnisse für die Entscheidungsfindung und den Wettbewerbsvorteil gewinnen.

Unmittelbar vorbereitende Schritte

Beginnen Sie mit einer vorläufigen CO₂-Fußabdruck , um die Emissionsquellen und die Datenverfügbarkeit Ihrer Organisation zu verstehen. Diese diagnostische Übung deckt Lücken in den Datenerfassungssystemen auf, identifiziert wichtige Emissions-Hotspots und liefert ein grundlegendes Verständnis für die Festlegung von Zielen. Selbst grobe Berechnungen helfen bei der Priorisierung von Vorbereitungsmaßnahmen.

Richten Sie ein funktionsübergreifendes Team ein, das Fachwissen aus den Bereichen Nachhaltigkeit, Betrieb, Finanzen, Beschaffung und IT vereint. CO₂-Bilanzierung berührt jede Unternehmensfunktion und erfordert die Koordination zwischen traditionell getrennten Abteilungen. Weisen Sie klare Rollen für die Datenerfassung, die Überwachung der Berechnungen und die Erstellung von Berichten zu, um sicherzustellen, dass nichts durch organisatorische Risse fällt.

Entwicklung der Dateninfrastruktur

Eine solide CO₂-Reporting erfordert eine systematische Datenerfassung und Managementprozesse. Viele Organisationen stellen fest, dass ihre derzeitigen Systeme nicht die granularen Informationen erfassen, die für eine genaue CO₂-Bilanzierung erforderlich sind, insbesondere für scope 3 , die die Einbeziehung von Lieferanten und die Transparenz der Lieferkette erfordern.

Beginnen Sie mit der Verbesserung der Datenerfassung für scope 1 und scope 1 , die die klarsten Messwege bieten. Installieren Sie Energieüberwachungssysteme, verbessern Sie die Reisebuchungsverfahren, um emissionsrelevante Informationen zu erfassen, und erstellen Sie regelmäßige Datenerfassungspläne. Diese Grundlagen unterstützen eine genaue Berichterstattung und fördern gleichzeitig die Kohlenstoffkompetenz der Organisation.

Beginnen Sie bei der Vorbereitung auf scope 3 frühzeitig mit der Einbindung von Lieferanten. Große Unternehmen müssen ab 2028 scope 3 melden, aber der Aufbau von Lieferantenbeziehungen und Datenerfassungsprozessen braucht Zeit. Beginnen Sie mit den Hauptlieferanten, die den größten Anteil an den Beschaffungsausgaben haben, und erweitern Sie den Erfassungsbereich schrittweise, wenn die Systeme ausgereift sind.

Die Datenerfassungsplattform vonPlan A automatisiert einen Großteil dieses Prozesses mit einer intelligenten Datenzuordnung, die aus Ihren Uploads lernt und sich in bestehende Geschäftssysteme integrieren lässt. Die API der Plattform ermöglicht einen nahtlosen Datentransfer, während KI-gesteuerte Tools relevante Informationen aus Rechnungen, Rechnungen und Lieferantenberichten extrahieren.

Pläne und Ziele zur Gebäudereduzierung

Die spanische Verordnung verlangt quantifizierte Fünfjahrespläne zur Emissionsreduzierung, die die Organisationen über die Messung hinaus zu konkreten Maßnahmen drängen. Wirksame Pläne zeigen Möglichkeiten zur Emissionsreduzierung auf, quantifizieren die potenziellen Auswirkungen und legen Zeitpläne für die Umsetzung mit klaren Maßnahmen zur Rechenschaftslegung fest.

Beginnen Sie die Zielsetzung mit wissenschaftlich fundierten Ansätzen, die mit Spaniens nationalen Klima und internationalen Vereinbarungen übereinstimmen. Die Verordnung fördert die Angleichung an die Methodik Science Based Targets initiative (SBTi) , um sicherzustellen, dass die Ziele einen sinnvollen Beitrag zu den globalen Dekarbonisierung leisten und gleichzeitig realistisch bleiben.

Die Zielentwicklung sollte berücksichtigen:

- Absolute Emissionsreduktionen in allen Bereichen

- Intensitätsbasierte Ziele, die Emissionen mit Geschäftswachstumskennzahlen verknüpfen

- Zwischenziele, die eine Fortschrittskontrolle und Kurskorrektur ermöglichen

- Finanzielle Auswirkungen, einschließlich Investitionsbedarf und betriebliche Einsparungen

- Anforderungen an die Einbindung der Lieferkette für scope 3

- Technologie-Roadmaps für wichtige Initiativen Dekarbonisierung

Einsatz von Technologie für die Einhaltung von Vorschriften

Moderne Plattformen für CO₂-Bilanzierung reduzieren den Verwaltungsaufwand für die Einhaltung gesetzlicher Vorschriften erheblich und bieten gleichzeitig strategische Einblicke zur Verbesserung des Geschäfts. Diese Lösungen automatisieren die Datenerfassung, stellen die Genauigkeit der Berechnungen sicher und erstellen Berichte, die den spanischen gesetzlichen Anforderungen entsprechen.

Die Plattform vonPlan A bietet besondere Vorteile für die Einhaltung spanischer Vorschriften, darunter:

- Spanienspezifische Emissionsfaktoren, die das lokale Energienetz und Verkehrssystem widerspiegeln

- KI-gestützte Einblicke, die Möglichkeiten zur Senkung der Kosten und finanzielle Auswirkungen aufzeigen

- Tools zur Einbindung von Lieferanten, die die Erhebung von scope 3 erleichtern

Die Messfunktionen der Plattform gewährleisten eine genaue Berechnung über alle Emissionsbereiche hinweg und bieten gleichzeitig die für eine effektive Planung der Emissionsreduzierung erforderliche granulare Analyse. Die integrierte Verifizierungsunterstützung bereitet Unternehmen auf die Anforderungen von Dritten vor.

Beginnen Sie jetzt mit Ihrer Scope 1 und 2 Berichterstattung

Spaniens neue CO₂-Reporting schaffen sowohl Herausforderungen als auch Chancen für Unternehmen, die bereit sind, eine systematische Dekarbonisierung zu betreiben. Vor allem aber schafft sie ein Gefühl der Dringlichkeit.

Unternehmen, die sich gründlich vorbereiten, in geeignete Systeme investieren und echte Fähigkeiten zur Reduktion entwickeln, werden in einem zunehmend kohlenstoffbewussten Markt Wettbewerbsvorteile haben. Diejenigen, die die Einhaltung der Vorschriften als reine Pflichtübung betrachten, laufen Gefahr, die strategischen Vorteile eines umfassenden CO₂-Management zu verpassen.

Fordern Sie eine Demo an und erfahren Sie, wie die Plattform und das Fachwissen von Plan A Ihre spanische CO₂-Reporting optimieren und gleichzeitig die Grundlage für einen langfristigen Dekarbonisierung schaffen kann. Da die gesetzlichen Fristen schnell näher rücken, sorgt eine frühzeitige Vorbereitung für eine reibungslose Einhaltung der Vorschriften und positioniert Ihr Unternehmen für eine führende Rolle in Spaniens sich entwickelnder nachhaltiger Unternehmenslandschaft.

.jpg)