In der sich entwickelnden Landschaft von Unternehmerische Nachhaltigkeit gewinnt das Konzept der "vermiedenen Emissionen" oder Scope 4-Emissionen neben den traditionellen Treibhausgas Emissionskategorien des Treibhausgas Protokolls (GHG Protocol) an Bedeutung.

Während Scope 1 direkte Emissionen aus eigenen oder kontrollierten Quellen abdeckt, umfasst Scope 2 indirekte Emissionen aus der Erzeugung von gekaufter Energie und Scope 3 alle anderen indirekten Emissionen innerhalb der Wertschöpfungskette eines Unternehmens. Scope 4 führt eine neue Dimension ein, indem es sich auf Emissionsreduktionen konzentriert, die durch die Verwendung von Produkten oder Dienstleistungen eines Unternehmens erreicht werden. Diese aufstrebende Kategorie, obwohl noch nicht offiziell vom GHG-Protokoll anerkannt, gewinnt zunehmend an Bedeutung für Unternehmen, die ein umfassendes Verständnis ihrer Umweltauswirkungen anstreben.

Was sind vermiedene Emissionen im Scope 4?

Die Emissionen des Scope 4, auch bekannt als 'vermiedene Emissionen', stellen ein relativ neues Konzept in Bezug auf Umweltschutz und CO₂-Bilanzierung dar. Dieser Begriff wurde 2013 vom World Resources Institute eingeführt und bietet eine neue Perspektive zur Messung des Einflusses eines Unternehmens auf Treibhausgas (THG)-Emissionen. Im Gegensatz zu den traditionellen Scopes (Scope 1, 2 und 3), die sich auf Emissionen direkt oder indirekt im Zusammenhang mit den Betriebsabläufen und der Wertschöpfungskette eines Unternehmens konzentrieren, berücksichtigen Scope 4-Emissionen die Reduzierung von Emissionen, die durch die Nutzung eines Produkts oder einer Dienstleistung entstehen.

Beispiel für Scope 4-Emissionen

Beispiele für Produkte, die zu Scope 4-Emissionen beitragen, sind Niedrigtemperatur-Waschmittel, spritsparende Reifen oder Telekonferenzgeräte und -dienste. Diese Produkte tragen mit ihrer Effizienz oder Funktionalität zur Reduzierung der gesamten Treibhausgasemissionen bei. Zum Beispiel reduzieren Telekonferenzdienste die Notwendigkeit zu reisen und vermeiden somit Emissionen, die sonst entstanden wären.

Die Toaster-Analogie

Bildnachweis: Unsplash

Um dies zu veranschaulichen, betrachten wir den Fall eines Toaster-Herstellers. Wenn das Unternehmen Innovationen vorantreibt, um einen energieeffizienteren Toaster zu entwickeln, werden die durchschnittlichen CO2-Emissionen pro Toastscheibe reduziert. Allerdings könnten die gesamten Scope 3-Emissionen des Unternehmens (Kategorie 11, die den Verkauf von Produkten einschließt) aufgrund höherer Verkaufszahlen steigen. In diesem Szenario fallen die pro Nutzung des Toasters reduzierten Emissionen (aufgrund gesteigerter Effizienz) unter die Scope 4-Emissionen. Dies sind die vermiedenen Emissionen aufgrund der Investition des Unternehmens in Forschung und Entwicklung, die zu einem effizienteren Produktdesign führt, selbst wenn das Gesamtvolumen der Verkäufe steigt.

Warum ist Scope 4 wichtig?

Scope 4-Emissionen bieten einen umfassenderen Überblick über die Umweltauswirkungen eines Unternehmens und heben die positiven Externalitäten seiner Produkte oder Dienstleistungen hervor. Dieser Aspekt der CO₂-Bilanzierung ist entscheidend, um das vollständige Spektrum des CO₂-Fußabdrucks eines Unternehmens und seinen Beitrag zur Erreichung einer klimaneutralen Wirtschaft zu verstehen. Die Berichterstattung über Scope 4-Emissionen erfasst daher nicht nur die Emissionen, für die ein Unternehmen direkt oder indirekt verantwortlich ist, sondern auch die Emissionen, die durch seine Produkte oder Dienstleistungen verhindert werden.

Welche Unternehmen berichten über Scope-4-Emissionen?

Einige zukunftsorientierte Unternehmen in verschiedenen Branchen haben begonnen, die Bedeutung von Scope 4-Emissionen in ihrem Umweltberichterstattung zu erkennen. Diese Unternehmen sind Vorreiter bei der Erfassung der positiven Umweltauswirkungen ihrer Produkte und Dienstleistungen, über die traditionellen Scope 1, 2 und 3-Emissionen hinaus.

Derzeit gibt es keine weit verbreitete, standardisierte Praxis zur Berichterstattung über Scope 4-Emissionen, da dieses Konzept noch nicht formell in das Treibhausgasprotokoll integriert ist. Unternehmen, die führend in Nachhaltigkeit und Umweltinnovation sind, beginnen jedoch damit, diese Emissionen zu erkunden und informell zu erfassen.

Diese Early Adopters sind in der Regel in Branchen zu finden, in denen Produkte und Dienstleistungen einen direkten Einfluss auf die Reduzierung von Treibhausgasemissionen haben. Beispiele hierfür sind:

Frühzeitige Anwender und Branchenführer

- Unternehmen für erneuerbare Energien: Unternehmen im Bereich erneuerbare Energien, wie Hersteller von Solarmodulen oder Windturbinen, sind wahrscheinliche Kandidaten für die Berichterstattung über Scope 4-Emissionen, da ihre Produkte direkt zur Reduzierung der Abhängigkeit von fossilen Brennstoffen beitragen.

Beispielsweise hat Renewable Energy Global mit Sitz in Indien konkrete Zahlen zu vermiedenen Emissionen veröffentlicht. Solche Offenlegungen spiegeln einen wachsenden Trend multinationaler Unternehmen wider, ihre umfassenderen Umweltauswirkungen zu erfassen und darüber zu berichten - Hersteller von Technologie und Elektronik: Unternehmen, die energieeffiziente Geräte, umweltfreundliche Gadgets und fortschrittliche Materialien herstellen, die zu Energieeinsparungen beitragen, können potenzielle Berichterstatter von Scope 4-Emissionen sein.

Zum Beispiel hat sich das FTSE 100-Technologieunternehmen Aveva verpflichtet, bis 2025 eine Grundlinie und ein Ziel für Kunden-gesparte und vermiedene Emissionen zu entwickeln, die es als Scope 4 bezeichnet. Dieser Schritt zeigt eine strategische Ausrichtung auf die breitere Auswirkung ihrer Produkte und Dienstleistungen auf die Reduzierung von Emissionen. - Automobilindustrie: Hersteller von Elektrofahrzeugen und Unternehmen, die kraftstoffeffiziente Fahrzeuge oder Komponenten produzieren, dürften auch die Scope-4-Emissionen in ihren Umweltberichten berücksichtigen.

- Bauwesen und nachhaltiges Bauen: Unternehmen, die sich mit nachhaltigen Baumaterialien, energieeffizienten Bautechnologien und grüner Architektur beschäftigen, können die Emissionen des Scope 4 durch den reduzierten Energieverbrauch ihrer Projekte erfassen.

- Logistiksektor: Wie von Branchenexperten festgestellt wurde, ist der Logistiksektor besonders aktiv bei der Einführung von Scope 4-Berichterstattung. Transportunternehmen konzentrieren sich zunehmend auf die Kraftstoffeffizienz von Lastwagen und die damit verbundene Reduzierung des CO₂-Fußabdrucks von Lieferungen und betonen die Rolle der betrieblichen Effizienz bei der Verringerung der Gesamtemissionen

Die Rolle von Investmentfirmen und Aktionären

- Investmentanalyse: Investmentfirmen wie Schroders beziehen vermiedene Emissionen in ihre Investmentanalysen ein. Diese Entwicklung deutet darauf hin, dass der Finanzsektor beginnt, den Wert von Scope 4-Emissionen bei der Bewertung der Gesamt-Nachhaltigkeitsleistung eines Unternehmens zu erkennen.

- Impact-Investoren: Diese Investoren, die positive soziale oder Umweltauswirkungen anstreben, beziehen häufig vermiedene Emissionen als wichtige Kennzahl in ihre Bewertung eines Unternehmens ein. Ihr Fokus auf Scope 4-Emissionen spiegelt eine sich entwickelnde Investitionslandschaft wider, in der Umweltauswirkungen eine bedeutende Rolle bei Investitionsentscheidungen spielen.

Richtlinien für Berichterstattung und zukünftige Trends

Das World Resources Institute (WRI) empfiehlt Unternehmen, sich zunächst auf die Berechnung und Berichterstattung ihrer Scope 1, 2 und 3 Emissionen zu konzentrieren, um ein umfassendes Verständnis ihres Gesamtemissionsprofils zu erlangen. Dieser grundlegende Schritt ist entscheidend, bevor man sich mit den Scope 4 Emissionen befasst, die die vermiedenen Emissionen darstellen.

Darüber hinaus wird erwartet, dass sich die Berichtsstandards weiterentwickeln, insbesondere aufgrund der gestiegenen Erwartungen des Task Force on Climate-related Financial Disclosures (TCFD) und des International Sustainability Standards Board (ISSB). Es wird erwartet, dass immer mehr Organisationen beginnen, Scope 4-Emissionen zu messen und zu berichten. Diese Veränderung soll parallel zur zunehmenden Berichterstattung über Scope 3-Emissionen an Bedeutung gewinnen und stellt einen bedeutenden Fortschritt in der Landschaft der Umweltverantwortung und Transparenz dar.

Während das Konzept der Scope-4-Emissionen vielversprechend ist, birgt es auch Herausforderungen, insbesondere in Bezug auf Messung und Standardisierung. Mit der Weiterentwicklung der Umweltberichterstattung ist zu erwarten, dass immer mehr Unternehmen die Berichterstattung über Scope-4-Emissionen übernehmen, getrieben von der steigenden Nachfrage der Stakeholder nach Transparenz und Verantwortlichkeit in Bezug auf Umweltauswirkungen. Die Entwicklung standardisierter Methoden und Rahmenbedingungen für die Berichterstattung über Scope-4-Emissionen wird entscheidend sein, um eine breitere Akzeptanz bei Unternehmen zu fördern.

Methoden zur Berechnung der vermiedenen Emissionen eines Unternehmens

Die Berechnung von Scope 4-Emissionen oder "vermiedenen Emissionen" erfordert einen differenzierten Ansatz, um den Einfluss der Produkte oder Dienstleistungen eines Unternehmens auf die Reduzierung der gesamten Treibhausgasemissionen genau zu erfassen. Zwei unterschiedliche Methoden, konsequentiell und attributiv, bieten verschiedene Perspektiven, durch die diese Emissionen bewertet werden können.

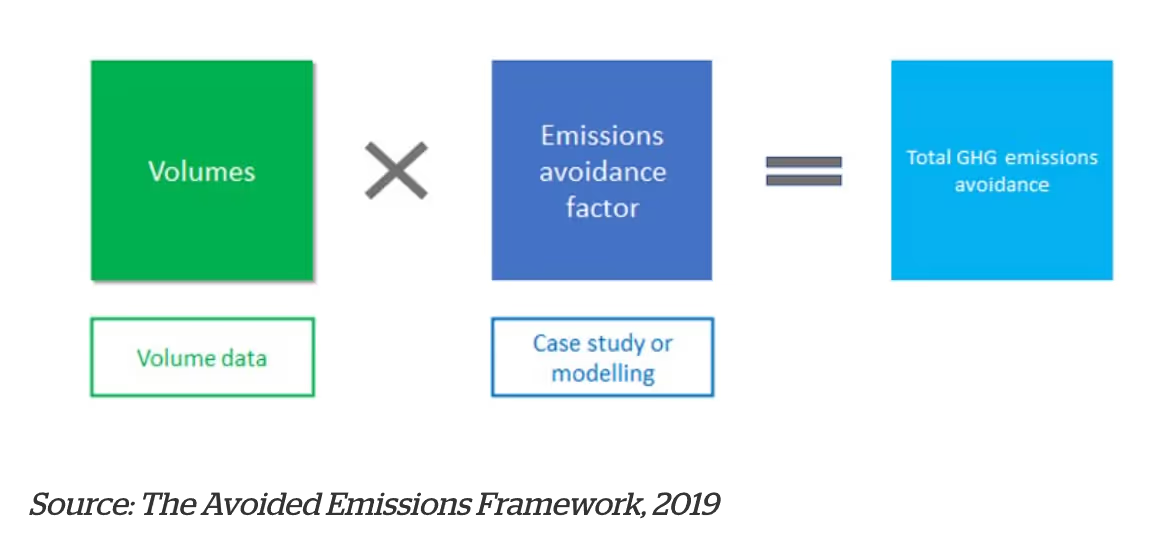

Gutschrift: Der Rahmen für vermiedene Emissionen

Konsequenter Ansatz

Der konsequenzenorientierte Ansatz zur Berechnung von Scope-4-Emissionen umfasst die Bewertung der systemweiten Veränderung der Emissionen, die durch eine bestimmte Entscheidung oder Maßnahme verursacht wird. Diese Methode ist ganzheitlich, da sie nicht nur die direkten Auswirkungen der Nutzung eines Produkts betrachtet, sondern auch seine sekundären Effekte und möglichen unbeabsichtigten Konsequenzen. Wenn beispielsweise ein Unternehmen ein neues, energieeffizienteres Gerät einführt, würde der konsequenzenorientierte Ansatz die gesamte Emissionsreduktion im Gesamtsystem bewerten, wie etwa im Energieversorgungsnetz, die durch die weit verbreitete Übernahme dieses Geräts resultiert. Diese Methode erfordert eine umfassende Analyse der Umweltauswirkungen des Produkts im weiteren Kontext und berücksichtigt verschiedene Faktoren wie Marktdynamik, Verbraucherverhalten und potenzielle Veränderungen in Industriepraktiken.

Ansatz der Zuordnung

Im Gegensatz dazu konzentriert sich der attributive Ansatz auf die absoluten Emissionen und Entfernungen, die mit einem Produkt im Vergleich zu einem Referenz- oder Baseline-Produkt verbunden sind. Diese Methode ist einfacher und wird aufgrund ihrer Praktikabilität häufig verwendet, insbesondere wenn es Einschränkungen in Bezug auf die Verfügbarkeit von Informationen oder Zeit gibt. Zum Beispiel würde der attributive Ansatz bei einem Elektrofahrzeug die während seines Lebenszyklus (einschließlich Herstellung, Nutzung und Entsorgung) produzierten Emissionen mit denen eines herkömmlichen benzinbetriebenen Fahrzeugs vergleichen. Der Unterschied in den Emissionen zwischen den beiden Produkten stellt die Scope 4-Emissionen dar, oder die vermiedenen Emissionen aufgrund der Verwendung des Elektrofahrzeugs anstelle der konventionellen Alternative.

Beide Ansätze haben ihre Vorzüge und können je nach dem spezifischen Kontext des Unternehmens und seiner Produkte ausgewählt werden. Der konsequente Ansatz bietet ein umfassenderes Verständnis der Umweltauswirkungen eines Produkts, kann jedoch komplex und datenintensiv sein. Der attributive Ansatz ist zwar in seinem Umfang begrenzter, erlaubt jedoch eine direktere und leichter quantifizierbare Beurteilung vermiedener Emissionen.

Letztendlich hängt die Wahl zwischen diesen Methoden von den Zielen des Unternehmens, der Art seiner Produkte und der Verfügbarkeit von Daten und Ressourcen ab.

Beste Praktiken in Bezug auf Scope 4-Emissionen

Wenn es um die Berichterstattung von Scope 4-Emissionen geht, bewegen sich Unternehmen in relativ neuem Terrain ohne standardisierte Methodik. Es haben sich jedoch mehrere bewährte Verfahren herausgebildet, die Organisationen bei der genauen Berechnung und Berichterstattung dieser Emissionen unterstützen können. Diese Verfahren gewährleisten nicht nur Transparenz und Genauigkeit, sondern erhöhen auch die Glaubwürdigkeit der Umweltberichterstattung des Unternehmens.

Durch die Anwendung dieser bewährten Verfahren können Unternehmen die Komplexität der Berechnung und Berichterstattung von Scope-4-Emissionen effektiv bewältigen. Diese Praktiken gewährleisten nicht nur einen verantwortungsbewussten Ansatz für die Umweltberichterstattung, sondern tragen auch zu einem genaueren und umfassenderen Verständnis des Beitrags eines Unternehmens zur Reduzierung der Gesamtemissionen bei.

Ist es obligatorisch, Scope 4-Emissionen zu berechnen und zu melden?

Derzeit ist die Berichterstattung von Scope-4-Emissionen nicht verpflichtend. Das Treibhausgas-Protokoll (GHG Protocol), das den Standard für Emissionsberichte setzt, hat Scope 4 bislang noch nicht offiziell anerkannt. Dennoch kann eine freiwillige Berichterstattung dieser Emissionen einen umfassenderen Überblick über die Umweltauswirkungen eines Unternehmens sowie deren Fortschritte in Sachen Nachhaltigkeit bieten.

Was sind Scope-1-, Scope-2- und Scope-3-Emissionen?

Die Emissionen der Scopes 1, 2 und 3 sind unterschiedliche Kategorien in der Berichterstattung über Treibhausgase, die sich deutlich von den Emissionen des Scope 4 unterscheiden:

- Scope 1: Dabei handelt es sich um direkte Emissionen aus Quellen, die dem Unternehmen gehören oder von ihm kontrolliert werden, wie beispielsweise Emissionen von Firmenfahrzeugen und Produktionsanlagen.

- Scope 2: Diese Emissionen stammen aus indirekten Quellen, insbesondere der Erzeugung von zugekauftem Strom, Dampf, Heizung und Kühlung, die das Unternehmen nutzt.

- Scope 3: Diese Kategorie umfasst alle anderen indirekten Emissionen, die innerhalb der gesamten Wertschöpfungskette des Unternehmens auftreten, sowohl vorgelagert (z. B. aus der Produktion von eingekauften Materialien) als auch nachgelagert (z. B. aus der Nutzung verkaufter Produkte).

Im Gegensatz dazu beziehen sich Scope 4-Emissionen auf die Reduzierung von Emissionen, die durch die Verwendung von Produkten oder Dienstleistungen eines Unternehmens erreicht wird. Während sich Scope 1, 2 und 3 auf Emissionen konzentrieren, die direkt und indirekt durch die Geschäftstätigkeit des Unternehmens entstehen, hebt Scope 4 die positive Umweltauswirkung seiner Produkte oder Dienstleistungen hervor.

Welche Vorteile bietet die Berechnung von Scope 4-Emissionen?

Die Berechnung von Scope 4-Emissionen bietet mehrere Vorteile:

- Globale Betrachtung der Auswirkungen: Bietet ein umfassendes Bild der Umweltauswirkungen eines Unternehmens, einschließlich der positiven Effekte seiner Produkte und Dienstleistungen.

- Innovationsantrieb: Fördert Innovationen in der Produkt- und Dienstleistungsgestaltung mit Fokus auf Nachhaltigkeit, was zu einer Verringerung der Umweltauswirkungen führt.

- Reputationserhöhung: Zeigt das Engagement eines Unternehmens für umfassende Umweltverantwortung, was den Ruf des Unternehmens verbessert.

- Informierte Entscheidungsfindung: Hilft dabei, die weitreichenden Auswirkungen von Geschäftstätigkeiten zu verstehen und Entscheidungen über nachhaltige Projekte und Investitionen zu lenken.

- Strategische Partnerschaften: Hilft bei der Auswahl von Lieferanten und Partnern, die mit den Nachhaltigkeitszielen übereinstimmen, um insgesamt positive Umweltauswirkungen zu erzielen.

- Technologischer Fortschritt: Forschung und Entwicklung von Kraftstoffen, die nicht nur Emissionen reduzieren, sondern auch zu deren Vermeidung beitragen.

Die Messung von Scope 4-Emissionen bringt Unternehmen in Einklang mit ehrgeizigeren und ganzheitlichen Nachhaltigkeitszielen. Diese proaktive Haltung ist in der heutigen immer umweltbewussteren Geschäftswelt unerlässlich.

Gibt es eine Zukunft für Scope 4-Emissionen?

Trotz des wachsenden Interesses gibt es ein erhebliches Hindernis: Viele Unternehmen haben immer noch Schwierigkeiten, die Emissionen von Scope 1, 2 und insbesondere Scope 3 genau zu erfassen. Scope 3-Emissionen, die indirekte Emissionen in der Wertschöpfungskette eines Unternehmens abdecken, sind aufgrund ihrer umfangreichen und vielfältigen Natur äußerst komplex. Da Unternehmen immer noch daran arbeiten, diese Emissionen vollständig zu verstehen und effektiv zu berichten, könnte es mehrere Jahre dauern, bis Scope 4-Emissionen in die standardmäßige Berichterstattung integriert werden. Die Entwicklung und Einführung einer umfassenden Norm für Scope 4-Emissionen erfordert Zeit, gemeinsame Anstrengungen und Zusammenarbeit zwischen Branchen und Regulierungsbehörden.

Im Wesentlichen besteht das Potenzial, die Umweltstrategien von Unternehmen erheblich zu verbessern, während das Konzept der Scope-4-Emissionen in die standardmäßige Berichterstattung und die weit verbreitete Anwendung in verschiedenen Branchen integriert wird. Dieser Prozess wird voraussichtlich noch mehrere Jahre dauern. In dieser Zeit müssen die erforderlichen Standards, Methoden und die unternehmensweite Vertrautheit mit Berichterstattungspraktiken etabliert werden, die über den aktuellen Umfang der Emissionsbilanzierung hinausgehen.

Während sich die Diskussion über Scope 4-Emissionen weiterentwickelt, wird deutlich, dass das Verständnis und die Verwaltung des CO₂-Fußabdrucks eines Unternehmens wichtiger denn je sind. Für diejenigen, die in Sachen Nachhaltigkeit vorausbleiben möchten, bietet Plan A Expertenlösungen an. Buchen Sie noch heute eine Demo bei uns, um Ihren CO₂-Fußabdruck zu berechnen und effektiv zu reduzieren. Dadurch stellen Sie sicher, dass Ihr Unternehmen nicht nur den Vorschriften entspricht, sondern auch eine Vorreiterrolle in Sachen Umweltverantwortung einnimmt.