In the evolving landscape of corporate sustainability, the concept of ‘avoided emissions’ or Scope 4 emissions is gaining prominence alongside the traditional greenhouse gas emissions categories identified by the Greenhouse Gas Protocol (GHG Protocol).

While Scope 1 covers direct emissions from owned or controlled sources, Scope 2 includes indirect emissions from the generation of purchased energy, and Scope 3 encompasses all other indirect emissions within a company's value chain, Scope 4 introduces a novel dimension by focusing on emissions reductions achieved through the use of a company’s products or services. This emerging category, although not yet officially recognised by the GHG Protocol, is becoming increasingly important for businesses seeking a comprehensive understanding of their environmental impact.

What are Scope 4 avoided emissions?

Scope 4 emissions, also known as ‘avoided emissions’, represent a relatively new concept in environmental sustainability and carbon accounting. This term was introduced by the World Resources Institute in 2013 and offers a novel perspective in measuring a company's impact on greenhouse gas (GHG) emissions. Unlike the traditional scopes (Scope 1, 2, and 3), which focus on emissions directly or indirectly associated with a company's operations and value chain, Scope 4 emissions take into account the reductions in emissions that occur as a result of the use of a product or service.

Example of Scope 4 emissions

Examples of products contributing to Scope 4 emissions include low-temperature detergents, fuel-saving tires, or teleconferencing equipment and services. These products, with their efficiency or functionality, help in reducing overall GHG emissions. For example, teleconferencing services reduce the need for travel, thereby avoiding emissions that would have otherwise occurred.

The toaster analogy

Credit: Unsplash

To illustrate, consider the case of a toaster manufacturer. If the company innovates to create a more energy-efficient toaster, the average CO2 emissions per slice of toast are reduced. However, the company’s total Scope 3 emissions (category 11, which includes the use of sold products) might increase due to higher sales. In this scenario, the emissions reduced per use of the toaster (due to enhanced efficiency) fall under Scope 4 emissions. These are the emissions avoided owing to the company's investment in research and development, leading to a more efficient product design, even if the total sales volume increases.

Why is Scope 4 important?

Scope 4 emissions provide a more comprehensive view of a company's impact on the environment, highlighting the positive externalities of its products or services. This aspect of carbon accounting is crucial for understanding the full spectrum of a company's carbon footprint and its contributions towards a net-zero economy. Reporting on Scope 4 emissions, therefore, captures not just the emissions a company is directly or indirectly responsible for, but also the emissions it helps to prevent through its products or services.

What companies report Scope 4 emissions?

Some forward-thinking companies across various sectors have begun to recognise the importance of Scope 4 emissions in their environmental reporting. These companies are pioneering in accounting for the positive environmental impact of their products and services, beyond the traditional Scope 1, 2, and 3 emissions.

Currently, there isn't a widespread, standardised practice for reporting Scope 4 emissions, as this concept is not yet formally integrated into the Greenhouse Gas Protocol. However, companies that are at the forefront of sustainability and environmental innovation are beginning to explore and informally account for these emissions.

These early adopters are typically found in industries where products and services have a direct impact on reducing greenhouse gas emissions. Examples include:

Early adopters and industry leaders

- Renewable energy companies: Firms in the renewable energy sector, such as solar panel or wind turbine manufacturers, are likely candidates for reporting Scope 4 emissions, as their products directly contribute to reducing reliance on fossil fuels.

For example, Renewable Energy Global, based in India is among the groups that has disclosed specific figures for avoided emissions. Such disclosures reflect a growing trend among multinational corporations to account for and report on their broader environmental impacts - Technology and electronics manufacturers: Companies producing energy-efficient appliances, eco-friendly gadgets, and advanced materials that contribute to energy savings are potential reporters of Scope 4 emissions.

For example, Aveva, a FTSE 100 tech company has committed to developing a baseline and target for customer-saved and avoided emissions, which it refers to as Scope 4, by 2025. This step indicates a strategic focus on the broader impact of their products and services on reducing emissions. - Automotive industry: Electric vehicle manufacturers and companies producing fuel-efficient vehicles or components are also likely to be considering Scope 4 emissions in their environmental reporting.

- Green building and construction: Firms involved in sustainable building materials, energy-efficient construction technologies, and green architecture may account for Scope 4 emissions through the reduced energy footprint of their projects.

- Logistics sector: As noted by industry experts, the logistics sector is particularly active in adopting Scope 4 reporting. Transport companies are increasingly focusing on lorries’ fuel efficiency and the associated reduction in the carbon footprint of deliveries, emphasising the role of operational efficiency in reducing overall emissions

The role of investment firms and shareholders

- Investment analysis: Investment firms such as Schroders are incorporating avoided emissions into their investment analyses. This shift suggests that the financial sector is beginning to recognise the value of Scope 4 emissions in assessing a company's overall sustainability performance.

- Impact investors: These investors, who seek positive social or environmental outcomes, often include avoided emissions as a key metric when determining the value of a company. Their focus on Scope 4 emissions reflects an evolving investment landscape where environmental impact plays a significant role in investment decisions.

Reporting guidelines and future trends

The World Resources Institute (WRI) recommends that companies should initially focus on calculating and reporting their Scope 1, 2, and 3 emissions to establish a comprehensive understanding of their total emissions profile. This foundational step is crucial before progressing to the consideration of Scope 4 emissions, which represent the avoided emissions.

Furthermore, as reporting standards evolve, particularly with heightened expectations from the Task Force on Climate-related Financial Disclosures (TCFD) and the International Sustainability Standards Board (ISSB), there is growing anticipation that more organisations will start to measure and report Scope 4 emissions. This shift is expected to gain momentum in parallel with the increasing prevalence of Scope 3 emissions reporting, marking a significant advancement in the landscape of environmental accountability and transparency.

While the concept of Scope 4 emissions is promising, it also presents challenges, particularly in terms of measurement and standardisation. As the environmental reporting landscape evolves, we can expect more companies to adopt Scope 4 emissions reporting, driven by increasing stakeholder demand for transparency and accountability in environmental impact. The development of standardised methodologies and frameworks for Scope 4 reporting will be crucial in encouraging more widespread adoption among businesses.

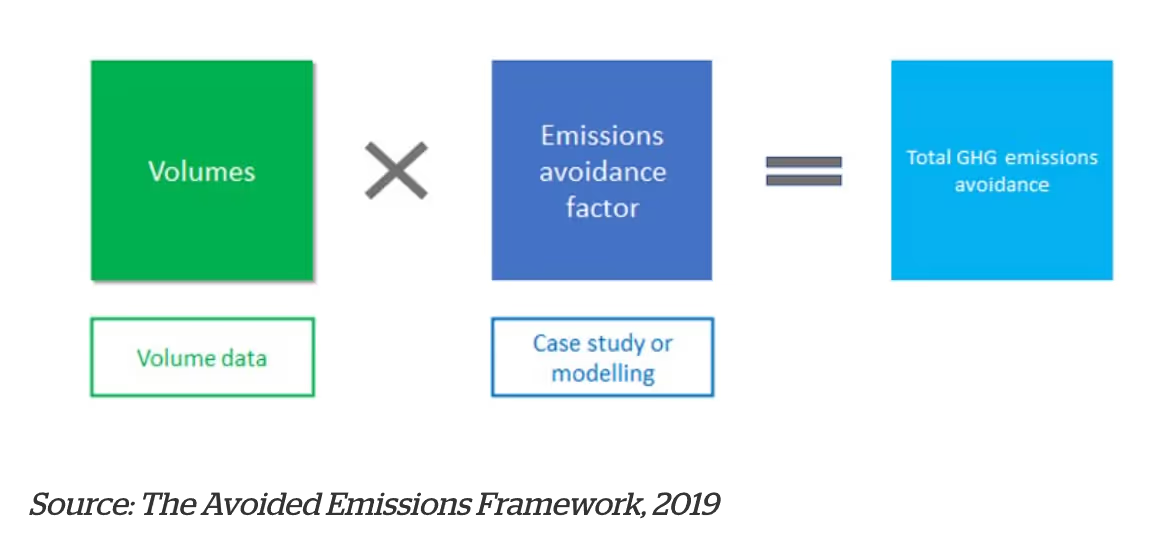

Methods to calculate a company’s avoided emissions

Calculating Scope 4 emissions, or 'avoided emissions', requires a nuanced approach to accurately capture the impact of a company's products or services on reducing overall greenhouse gas emissions. Two distinct methodologies, consequential and attributional, offer different lenses through which these emissions can be assessed.

Credit: The avoided emissions framework

Consequential approach

The consequential approach to calculating Scope 4 emissions involves assessing the system-wide change in emissions resulting from a specific decision or action. This method is holistic, as it considers not only the direct effects of a product's use but also its secondary impacts and potential unintended consequences. For instance, if a company introduces a new, more energy-efficient appliance, the consequential approach would evaluate the overall reduction in emissions in the entire system, such as the energy grid, resulting from the widespread adoption of this appliance. This method requires a comprehensive analysis of the product’s environmental impact within a broader context, considering various factors like market dynamics, consumer behaviour, and potential shifts in industry practices.

Attributional approach

In contrast, the attributional approach focuses on the absolute emissions and removals associated with a product, compared to a reference or baseline product. This method is more straightforward and is often used due to its practicality, especially when there are constraints related to information availability or time. For example, in the case of an electric vehicle, the attributional approach would compare the emissions produced during its lifecycle (including manufacturing, usage, and disposal) with those of a traditional gasoline-powered vehicle. The difference in emissions between the two products represents the Scope 4 emissions, or emissions avoided due to using the electric vehicle over the conventional alternative.

Both approaches have their merits and can be selected based on the specific context of the company and its products. The consequential approach offers a more comprehensive understanding of a product’s environmental impact, but it can be complex and data-intensive. The attributional approach, while more limited in scope, provides a more straightforward and readily quantifiable assessment of avoided emissions.

Ultimately, the choice between these methods depends on the company's objectives, the nature of its products, and the availability of data and resources.

Best practices regarding Scope 4 emissions

When it comes to reporting Scope 4 emissions companies are navigating relatively new territory without a standardised methodology. However, several best practices have emerged that can guide organisations in accurately calculating and reporting these emissions. These practices not only ensure transparency and accuracy but also enhance the credibility of the company’s environmental reporting.

By adopting these best practices, companies can effectively navigate the complexities of calculating and reporting Scope 4 emissions. These practices not only ensure a responsible approach to environmental reporting but also contribute to a more accurate and comprehensive understanding of a company’s contribution to reducing overall emissions.

Is it mandatory to calculate and report Scope 4 emissions?

Currently, reporting Scope 4 emissions is not mandatory. The GHG Protocol, which sets the standard for emissions reporting, has yet to officially recognise Scope 4. However, voluntary reporting of these emissions can provide a more comprehensive view of a company's environmental impact and progress in sustainability.

What are Scope 1, 2 and 3 emissions?

Scope 1, 2, and 3 emissions are distinct categories within greenhouse gas reporting that differ significantly from Scope 4 emissions:

- Scope 1: These are direct emissions from sources owned or controlled by the company, such as emissions from company vehicles and manufacturing facilities.

- Scope 2: These emissions stem from indirect sources, particularly the generation of purchased electricity, steam, heating, and cooling used by the company.

- Scope 3: This category includes all other indirect emissions that occur within the company’s entire value chain, both upstream (e.g., from the production of purchased materials) and downstream (e.g., from the use of sold products).

In contrast, Scope 4 emissions refer to the reduction in emissions achieved by the use of a company’s products or services. While Scopes 1, 2, and 3 focus on emissions produced directly and indirectly by the company's operations, Scope 4 highlights the positive environmental impact of its products or services.

What are the benefits of calculating Scope 4 emissions?

Calculating Scope 4 emissions offers several benefits:

- Holistic impact view: Offers a complete picture of a company's environmental impact, including the positive effects of its products and services.

- Innovation drive: Encourages innovation in product and service design focused on sustainability, leading to reduced environmental impacts.

- Reputation enhancement: Demonstrates a company’s commitment to comprehensive environmental stewardship, improving corporate reputation.

- Informed decision-making: Helps in understanding the broader implications of business activities, guiding decisions on sustainable projects and investments.

- Strategic partnerships: Aids in choosing suppliers and partners aligned with sustainability goals, enhancing overall environmental impact.

- Technological advancement: Fuels research and development towards solutions that not only reduce emissions but also contribute to avoiding them.

Measuring Scope 4 emissions aligns businesses with more ambitious and holistic sustainability goals. This proactive stance is essential in today's increasingly eco-conscious business landscape.

Is there a future for Scope 4 emissions?

Despite the growing interest, there's a significant roadblock: many companies are still grappling with accurately reporting Scope 1, 2, and especially Scope 3 emissions. Scope 3 emissions, which cover indirect emissions in a company's value chain, present considerable complexities due to their expansive and varied nature. As businesses are still working to fully comprehend and report these emissions effectively, the integration of Scope 4 emissions into standard reporting practices might take several years. The development and adoption of a comprehensive norm for Scope 4 emissions will require time, concerted effort, and collaboration across industries and regulatory bodies.

In essence, while the concept of Scope 4 emissions holds substantial potential for enhancing corporate environmental strategies, its full integration into standard reporting and widespread adoption across industries is a development that is likely several years away. This timeframe is necessary to establish the required standards, methodologies, and corporate familiarity with reporting practices that extend beyond the current scope of emissions accounting.

As the conversation around Scope 4 emissions continues to evolve, it's clear that understanding and managing a company's carbon footprint is more critical than ever. For those seeking to stay ahead in sustainability, Plan A offers expert solutions. Book a demo with us today to calculate and effectively reduce your carbon footprint, ensuring your business is not only compliant but also a leader in environmental stewardship.