Fill out the form below to access our summary document, with all the essential information you need.

REGULATION Centre

EU Taxonomy

The EU Taxonomy is a classification that sets criteria to determine whether an economic activity significantly contributes to the six environmental objectives defined in the regulation. It is a tool to help companies and investors make sustainable investment decisions. EU Taxonomy disclosures must be made as part of the NFRD/CSRD and SFDR reporting requirements.

The EU Taxonomy is a classification that sets criteria to determine whether an economic activity significantly contributes to the six environmental objectives defined in the regulation. It is a tool to help companies and investors make sustainable investment decisions. EU Taxonomy disclosures must be made as part of the NFRD/CSRD and SFDR reporting requirements.

What is the EU Taxonomy?

The EU Taxonomy is a classification that sets criteria to determine whether an economic activity significantly contributes to the six environmental objectives as defined in the regulation:

◦ Climate change mitigation

◦ Climate change adaptation

◦ Sustainable use and protection of water and marine resources

◦ Transition to a circular economy, including waste prevention and recycling

◦ Pollution prevention and control

◦ Protection of healthy ecosystems.

The EU Taxonomy is a tool to assist companies and investors in making sustainable investment decisions.

The EU Taxonomy is part of the EU Sustainable Finance Package, which aims to improve money flow towards sustainable activities across the European Union.

Which companies are subject to the EU Taxonomy?

The EU Taxonomy is mandatory for all companies offering financial products on the European market, including those in the scope of the EU Sustainable Finance Disclosure Regulation (SFDR) and those falling under the CSRD/NFRD.

Financial institutions in the scope of the EU SFDR

These entities will have to report on the level of Taxonomy alignment of their financial product as part of their EU SFDR product-related disclosures (pre-contractual and periodic disclosures).

Companies that have listed securities on an EU-regulated market

Non-EU companies (including EU subsidiaries of a UK parent) with annual revenue in the EU of > €150 million and an EU branch with a net income of > €40 million

Companies with at least one EU subsidiary (either a large EU company or an EU company listed on an EU-regulated market which isn't a micro undertaking) that fulfils at least two of the following three criteria):

more than 250 EU-based employees

balance sheet > €20 million

local revenue of > €40 million

What needs to be disclosed?

Due to the complexity of the EU Taxonomy and because part of the methodology still needs to be defined, the disclosure requirements for companies are being phased in over the next four years.

The final goal of the requirements is to:

Companies within the CSRD/NFRD scope must report the share of their "environmentally sustainable" economic activities (as defined by the EU Taxonomy) in their revenue, Capex, and OPEX.

Financial market participants will have to disclose how their financial products, within the scope of the SFDR, align with the EU Taxonomy.

Where to report?

Companies within the CSRD/NFRD's scope must report their Taxonomy disclosure in the annual CSRD/NFRD report, which must be published together with the company's management report.

The Taxonomy disclosure of companies in the scope of the SFDR needs to be published in periodic reviews and pre-contractual disclosures.

The current state of Taxonomy implementation

In addition to the CSRD reporting requirements, as of January 2022, the companies in scope must disclose the percentage of their economic activities that are eligible for the EU Taxonomy (for 2022).**

In addition to the SFDR requirements, as of January 2022, financial institutions must disclose the proportion of their total assets exposed to Taxonomy non-eligible and Taxonomy-eligible economic activities.

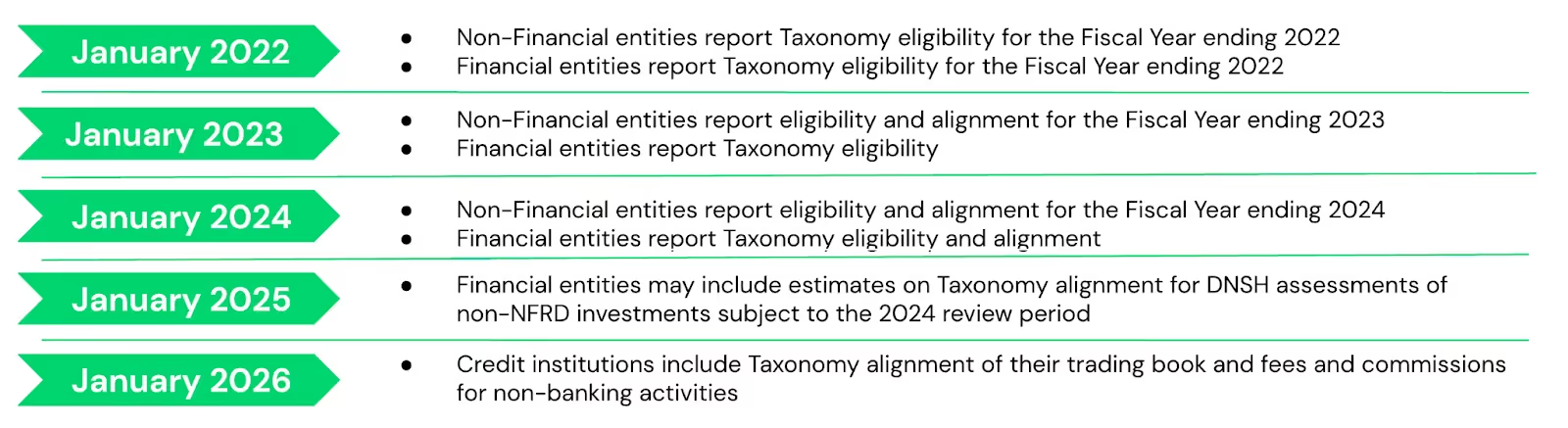

Timeline of disclosure requirements

From 2025 (for the FY 2024), companies will have to start disclosing their Taxonomy information as part of their non-financial report by the European Sustainability Reporting Standards (under the CSRD).

They will have to include the EU Taxonomy-aligned share of their turnover, capital expenditures (CapEx), and operating expenditures (OpEx) generated by their economic activities in their CSRD report.

Until then, non-financial companies in the scope of the CSRD/NFRD shall continue disclosing their Taxonomy information as part of their non-financial report to the CSRD/NFRD.

See more details in the diagram below:

The timeline of disclosure requirements for the EU Taxonomy Credit: Plan A

Will the disclosure requirements be externally assured?

The non-financial statements of companies in the scope of the CSRD/NFRD are subject to an existence check by the statutory auditor. The European Union Law does not require verifying the content of the disclosures. The statements are audited, now that the CSRD* is enforced.

The compliance of the disclosures of financial institutions that are subject to the SFDR will be monitored by competent authorities.

* The Corporate Sustainability Reporting Directive (CSRD) replaces the Non-Financial Reporting Directive (NFRD). With the CSRD, more companies are subject to reporting requirements, which the EU will define, and disclosures will be subject to external assurance. More information is here.

** Eligibility indicates that a company makes money in an activity that can be tested under the Taxonomy.

The clock is ticking! Start reporting on your impact today. Contact our policy experts to discover solutions adapted to your sustainability reporting needs.

Sustainability is a deep and broad ocean to navigate. Use my knowledge and intelligence to learn exponentially and find the right resources to make your case.

.webp)