.webp)

Internal carbon pricing (ICP) has become a staple tactic employed by businesses undergoing sustainable transformation. Businesses around the globe, including Plan A’s clients, are introducing internal carbon pricing measures to embed within its Key Performance Indicators (KPIs) a deep understanding of the risks and costs associated with their environmental impact.

What is internal carbon pricing?

An internal carbon price refers to a monetary value that companies place on greenhouse gas emissions, which businesses can then factor into investment decisions and business operations to drive positive change. Companies use internal carbon pricing as a strategic tool to manage climate-related business risks and prepare for a transition to a low-carbon economy. When a business sets an internal carbon price, a cost is typically assigned to each ton of carbon emitted so this can be factored into business and investment decisions, incentivising efficiency and enabling low-carbon innovation.

The wider concept of carbon pricing refers to an approach to reduce greenhouse gas (GHG) emissions by using market mechanisms to pass the cost of emissions onto emitters, usually by pricing the carbon dioxide equivalent (CO₂e) emitted. A carbon price works as an economic signal to polluters, and based on economic incentives, allows them to decide to either transform their activities, operate more sustainably and lower their emissions, or continue emitting and paying for their emissions.

What are the different mechanisms of internal carbon prices?

There are 3 commonly adopted approaches to internal carbon pricing:

- Shadow pricing: A shadow price refers to a monetary value a company assigns to its greenhouse gas (GHG) emissions on a per ton basis that is typically used to evaluate the potential cost/benefit of different emissions reduction strategies. No money is transferred with a shadow price.

- Internal carbon fee or charge: An internal carbon charge is a fee that a company charges itself on a per-ton basis that can be used to drive decision-making at the margin, reduce costs, or align internal culture with wider decarbonisation efforts. Internal fees are usually assessed at the business unit level or based upon specific emissions activities (e.g. electricity demand) and can be pooled for use in business-unit or corporate-wide sustainability efforts.

- Implicit carbon price: An implicit price is based on how much it costs the organisation to implement emission reduction projects. This is then applied to where GHG emissions are emitted within the business. A target may already be in place along with a program of investment. Meanwhile, several implicit carbon prices may appear within the same organisation. Businesses can strategically use the implicit price in sustainability communications and allocate costs across the business.

What factors are considered when setting an internally applied carbon price?

In setting the price, there are several points businesses must consider to ensure the price drives change, such as:

- External factors: Organisations must review external risks when calculating their carbon price, such as understanding variations in carbon tax risks across different countries. If an external tax risk is a driver, then the EU ETS should be included in the analysis. Another external factor might be the price of renewable energy certificates (RECs) and offsets.

- Internal factors: A key internal factor is the implicit cost of carbon for the organisation and the breakeven cost (the cost of carbon needed to make us choose option B over option A). Another key internal factor that must be considered is what price is needed to drive change.

Meanwhile, the entire company and each department must participate in an internal carbon pricing scheme. Accordingly, businesses have the choice to distribute responsibility for emission creation across departments depending upon their share of impact.

How to calculate your internal carbon price

Once your organisation has agreed upon the most appropriate mechanism to use to implement your internal carbon price, the carbon price must be calculated. Businesses must consider the aforementioned factors as they calculate their ICP in line with the methodology they utilise.

- Shadow price: Using the shadow price method, it is preferable to calculate your carbon price using external sources as a guide. This ensures that the carbon price accurately reflects the element of risk. Organisations may calculate their shadow price by linking to the cost of appropriate offsets or renewable energy certificates (RECs), or based on the costs of external mechanisms such as the EU Emissions Trading System (ETS) – particularly if an external tax risk is a driver.

- Internal carbon charge: The price of an internal carbon fee can be calculated based on the organisation's shadow price, implicit price, abatement costs, or external markets. The funds raised by this method would typically be reinvested into the businesses' decarbonisation efforts. Meanwhile, the price should be reviewed regularly to ensure it is positively impacting business decisions and sustainability goals.

- Implicit carbon price: An implicit price is calculated from an understanding of how much the company spends on reducing GHG emissions. Accordingly, businesses can calculate their implicit carbon price by developing an understanding of the costs incurred for implementing emissions reduction measures — which can be calculated via the abatement cost per ton of CO₂e.

Why is ICP becoming a trending business practice?

As businesses face exponential stakeholder and regulatory pressures to reduce their carbon emissions; all emissions within the supply chain pose significant risks. As such, businesses are integrating internal carbon pricing into their wider decarbonisation strategies to achieve their net-zero goals, and thus ascertain a strategic advantage. Some of the fundamental benefits of ICP schemes include:

- Driving internal decarbonisation: By putting a price on carbon, greater finance for sustainability initiatives will become available. Accordingly, the budget can be allocated towards climate-related technologies that promote the reduction of carbon emissions. For example, funds may be invested into research and development (R&D), carbon accounting software, or energy efficiency.

- Driving sustainability decision-making: By linking sustainability to a clear financial KPI, carbon emissions considerations become central to the long-term viability of the business. Meanwhile, it is far easier for decision-makers to evaluate the viability of current and future sustainability investments.

- Driving behavioural change: By establishing a budget based on emissions, businesses are incentivised to improve operational efficiency, foster innovation, and implement sustainable solutions across their wider value chain to future-proof their business.

- Highlighting climate risks and opportunities: Internal carbon prices are vital to communicating the risk of carbon to the business. By translating the potential impacts of not reducing emissions in terms that can be easily understood by high-level decision-makers, action will likely be taken to de-risk future carbon pressures and prices.

- Ensuring the demands of stakeholders are met: At the centre of pressures placed upon businesses to decarbonise are investors and consumers who demand transparency around climate action. Accordingly, making emissions output a financial liability demonstrates a great level of commitment that answers the sustainable demands of stakeholders.

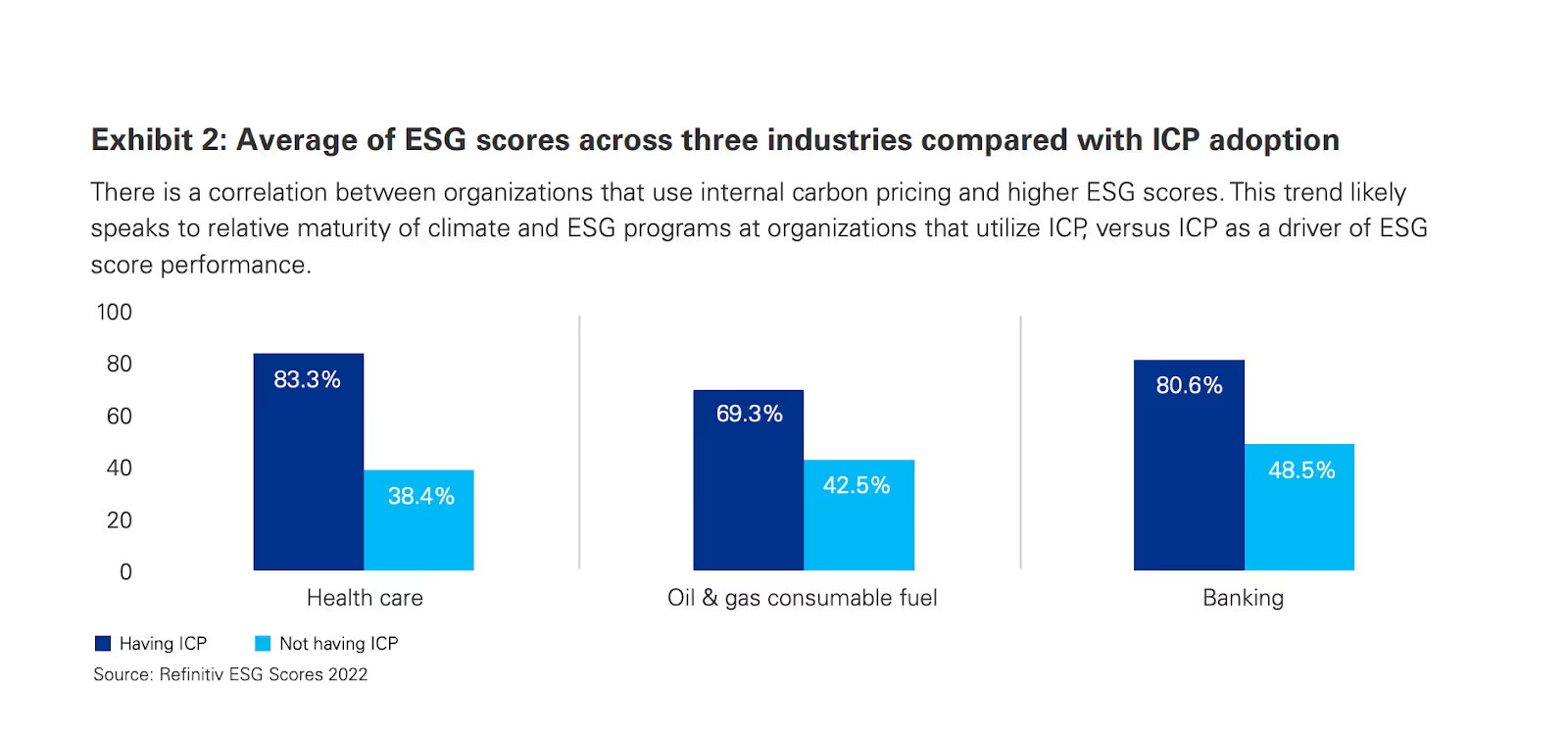

A positive correlation between internal carbon pricing and ESG scores.

Credit: KPMG

What are the internal carbon pricing standards?

There are currently no formal, defined global standards for the pricing of carbon emissions. Companies should select values that are most useful within their business contexts and regions. Meanwhile, businesses can use externally published sources such as the UK Green Book or CDP Carbon Pricing Corridors for guidance.

How to succeed in implementing an internal carbon pricing model

- Calculate your carbon footprint: Businesses must first conduct a thorough carbon footprint assessment to quantify their emissions. In line with the GHG Protocol, this involves collecting and measuring emissions data across scopes 1, 2 and 3.

- Establish reduction targets: Establishing decarbonisation targets is a critical aspect of any climate or decarbonisation strategy. Plan A can assist companies in setting science-based decarbonisation targets with the support of a team of leading carbon accounting experts.

- Get support and set carbon prices: Next, organisations must decide on the method that they will use to calculate the internal carbon price. When establishing a benchmark price for carbon within the organisation, businesses must consider external factors, such as carbon taxes, and internal factors, such as an estimation of the future cost of carbon. Once a pricing method has been established, businesses are then able to apply the chosen pricing method to their total emissions. For instance, they can multiply their emissions (in tons of CO₂e) by the internal carbon price per ton. This yields the internal cost of carbon for each emission source.

- Integrate carbon price into strategy and planning: Next, businesses must ensure that relevant stakeholders within the organisation are aware of the internal carbon price and its implications. This transparency is vital to building awareness and commitment to reducing carbon emissions. Organisations can use the internal carbon price as a factor in decision-making processes – such as factoring in the cost of carbon emissions when evaluating new investments,

- Monitor performance: Finally, businesses must regularly review and adjust the internal carbon price as necessary. Given that internal and external factors will affect the cost of carbon, such as regulatory changes or shifts in market prices, it is essential to reflect these changes in the organisation’s ICP.

Ultimately, the effectiveness of internal carbon pricing is highly dependent upon its integration into a company’s wider sustainability strategy, and the overall commitment of the organisation to reduce its carbon impact.

As such, businesses must consider implementing an internal carbon pricing method that directly affects financial performance to increase transparency and drive decision-making. Meanwhile, businesses must stay informed about developments in carbon markets and regulations that might impact their internal carbon price.