The Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS) have established comprehensive frameworks for greenhouse gas (GHG) emissions and carbon reporting. These guidelines aim to enhance sustainability reporting's transparency, consistency, and comparability.

In this article, we'll explain the GHG and carbon reporting requirements under CSRD and ESRS, providing a clear understanding of their implications and practical recommendations for compliance.

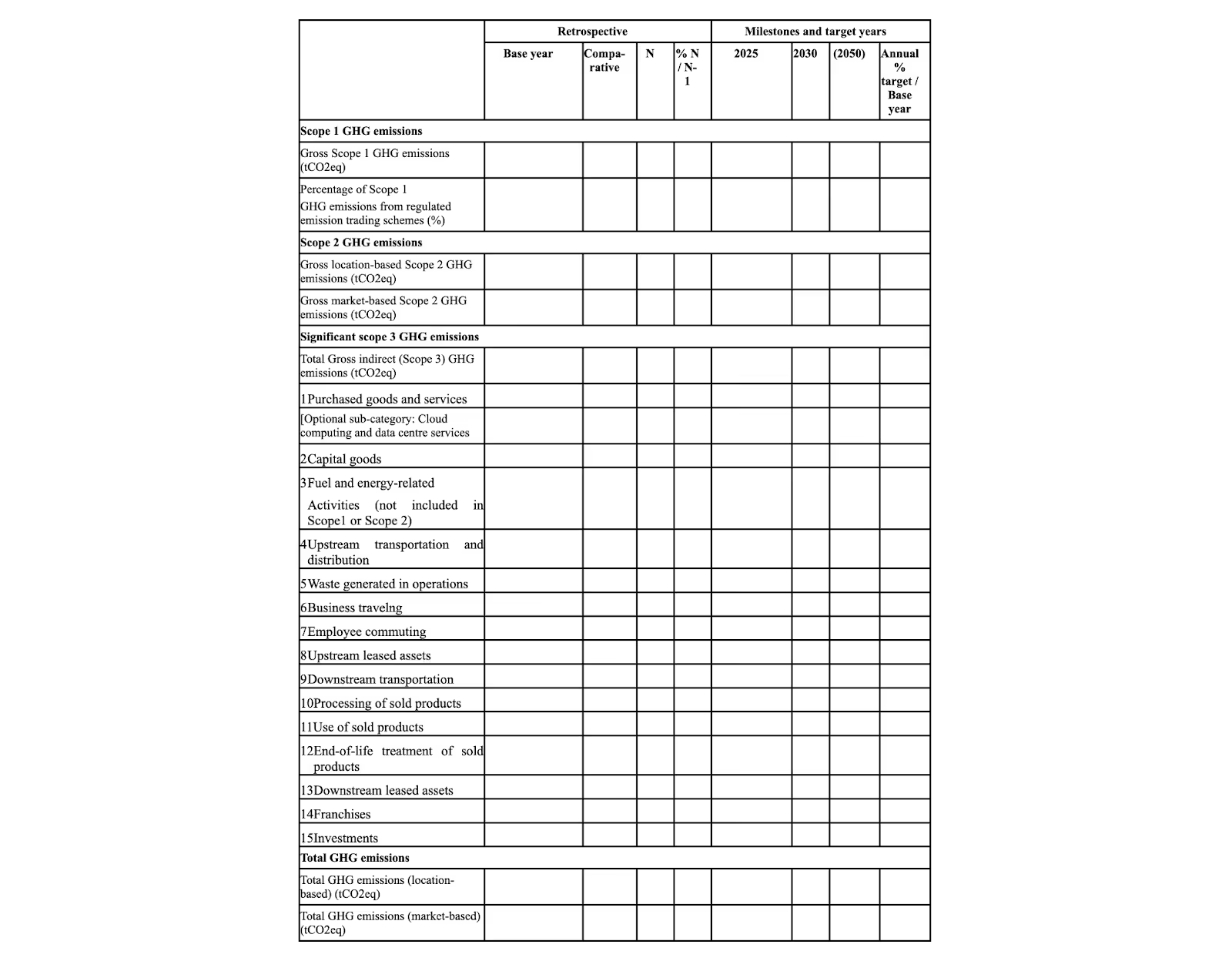

Understanding GHG reporting in the context of CSRD and ESRS

GHG reporting under CSRD and ESRS involves disclosing direct and indirect emissions across an organisation's value chain. The reporting requirements are categorised into Scopes 1, 2, and 3 emissions to provide a holistic view of an entity's carbon footprint.

- Scope 1 emissions: Direct emissions from owned or controlled sources.

- Scope 2 emissions: Indirect emissions from the generation of purchased electricity, steam, heating, and cooling consumed by the reporting entity.

- Scope 3 emissions: All other indirect emissions in a company's value chain.

Credit: Plan A

Key requirements under ESRS

The ESRS outlines specific disclosure requirements to ensure comprehensive GHG and carbon reporting:

Credit

Modern companies leverage carbon accounting software to manage their journey toward improved ESG performance and compliance with ESG regulations.

Practical guidance for CSRD and ESRS compliance

- Use recognised standards: Leverage established frameworks such as the GHG Protocol Corporate Standard, ISO 14064-1, and the GHG Protocol Scope 3 Standard for accurately measuring and reporting GHG emissions. These standards provide guidelines on boundaries, methodologies, and emission factors to ensure consistency and accuracy.

- Engage the value chain: Given the significance of Scope 3 emissions, collaborating with suppliers and downstream partners is crucial. Entities should work towards obtaining primary data from value chain partners to enhance the accuracy of Scope 3 emissions reporting.

- Integrate technology: Utilise technological tools for monitoring, calculating, and reporting GHG emissions. These tools can enhance data accuracy, streamline reporting processes, and provide real-time insights into the organisation's carbon footprint. Privilege carbon accounting software like Plan A.

- Regular updates and transparency: Entities should update their GHG emissions data to reflect significant changes in operations or the value chain. Transparent disclosure of methodologies, assumptions, and any use of carbon credits is required to maintain stakeholder credibility.

- Education and training: Ensure all relevant employees are well-informed about GHG reporting requirements and methodologies. Continuous training and updates on regulatory changes are essential to maintain compliance and improve reporting quality.

The detailed GHG and carbon reporting requirements under the CSRD and ESRS emphasise the importance of transparency and accountability in sustainability reporting. By adhering to these standards, entities can provide stakeholders with a clear and accurate view of their environmental impact, thereby contributing to broader climate action goals. Organisations can enhance their sustainability performance and foster stakeholder trust through diligent compliance and proactive engagement with value chain partners.

Explore Plan A's CSRD Manager via the interactive demo below:

Contact Plan A's team to get expert support and tools on sustainability reporting. Schedule a call today to discover our solutions.