The Carbon Border Adjustment Mechanism (CBAM) is an environmental policy designed to align the carbon price of imported goods with those produced domestically in the European Union to avoid so-called carbon leakage.

By incentivising decarbonisation through pricing carbon on imported products with high carbon content, CBAM is part of the EU’s “Fit for 55” strategy, aiming to reduce greenhouse gas (GHG) emissions by 55% by 2030 and achieve climate neutrality by 2050.

What is carbon leakage?

Carbon leakage occurs when companies relocate production from countries with strict greenhouse gas regulations (such as the EU with EU ETS) to those with more lenient policies, potentially increasing global emissions. While stricter policies may reduce emissions locally, they risk shifting emissions abroad as businesses seek lower costs and fewer regulations. In practice, the CBAM tries to correct for differences in emissions pricing between countries.

CBAM timeline and phases

Credit: Getty

Since October 2023, CBAM has been in its transitional phase, where reporting companies must submit quarterly reports to the EU Transitional Registry, an online portal administered by EU authorities. During this period, importers of goods in the scope of CBAM only have to report emissions embedded in their imports (direct and indirect emissions) without the need to buy and surrender certificates.

The objective of the transitional period is to serve as a pilot and learning period for all stakeholders (importers, producers and authorities) and to collect valuable information on embedded emissions to refine the methodology for the definitive period.

A review of the CBAM's functioning during its transitional phase will be concluded before the definitive system enters into force. At the same time, the product scope will be reviewed to assess the feasibility of including other goods produced in sectors covered by the EU ETS in the scope of the CBAM mechanism, such as certain downstream products and those identified as suitable candidates during negotiations. A timeline setting out their inclusion until 2030 will be published.

Scope of CBAM

CBAM will initially apply to import certain goods in industries whose production is carbon intensive and at most significant risk of carbon leakage, specifically these 6 sectors: cement, iron and steel, aluminium, fertilisers, electricity and hydrogen.

When fully phased in beyond 2030, CBAM is predicted to capture more than 50% of the emissions in EU ETS-covered sectors (such as glass, pulp & paper, ceramics, acids, bulk organic chemicals, waste, and potentially aviation and maritime).

Goods considered

.avif)

Credit: Getty

The CBAM Regulation applies to goods imported into the EU and is on the list of CN codes outlined by the regulation. CN codes (Combined Nomenclature) add two digits to the HS code (global product classification system) and are used as a commodity code for exports outside the EU.

The Commission has developed a CBAM Self Assessment Tool for Importers to the EU. The tool provides the possibility to get a quick overview of whether the imported goods are subject to CBAM during the transitional period, what the CBAM reporting requirements for that particular type of goods are, and where to find further information.

Some goods are exempt from CBAM, including imports valued under €150 per consignment (de minimis exemption), goods used by military authorities under EU or NATO agreements (military use exemption), and imports from countries like Norway and Switzerland that are already linked to the EU ETS (EFTA exemption).

The EU has opened a study into a potential CBAM scope extension to downstream goods and to other sectors and transport of CBAM goods. It aims to prioritise industries and products for expansion based on carbon leakage risk, emission relevance, technical feasibility, and administrative burden. The results of this study will feed into an informative report to co-legislators by mid-2025.

CBAM reporting and methodology

CBAM prescribes a specific methodology for calculating emissions, different from the GHG Protocol, product carbon footprint, or lifecycle assessment. Embedded emissions can be calculated using either a calculation-based approach, which relies on activity data and standard values, or a measurement-based approach, which measures GHG concentration and flow rate in flue gases.

During the transitional period until July 2024, importers can use default values for 100% of emissions. From mid-2024, default values can account for up to 20% of emissions for complex goods.

Step-by-step reporting guidelines

During the transitional period, i.e. until the end of 2025, as a reporting company:

- Define imported goods: Map goods to CN codes and define those in the scope of CBAM.

- Engage suppliers: Work with Tier 1 and 2 suppliers to obtain accurate emissions data.

- Submit reports: File quarterly reports detailing embedded emissions and associated parameters to the CBAM registry.

During the definitive period, starting 2026, reporting companies will have to do these additional steps:

- Verify data: Ensure emissions data align with CBAM’s guidelines, using third-party verification where required.

- Pay carbon price: Starting in 2026, the carbon tax will be calculated as embedded emissions x the average weekly cost of EU ETS allowances.

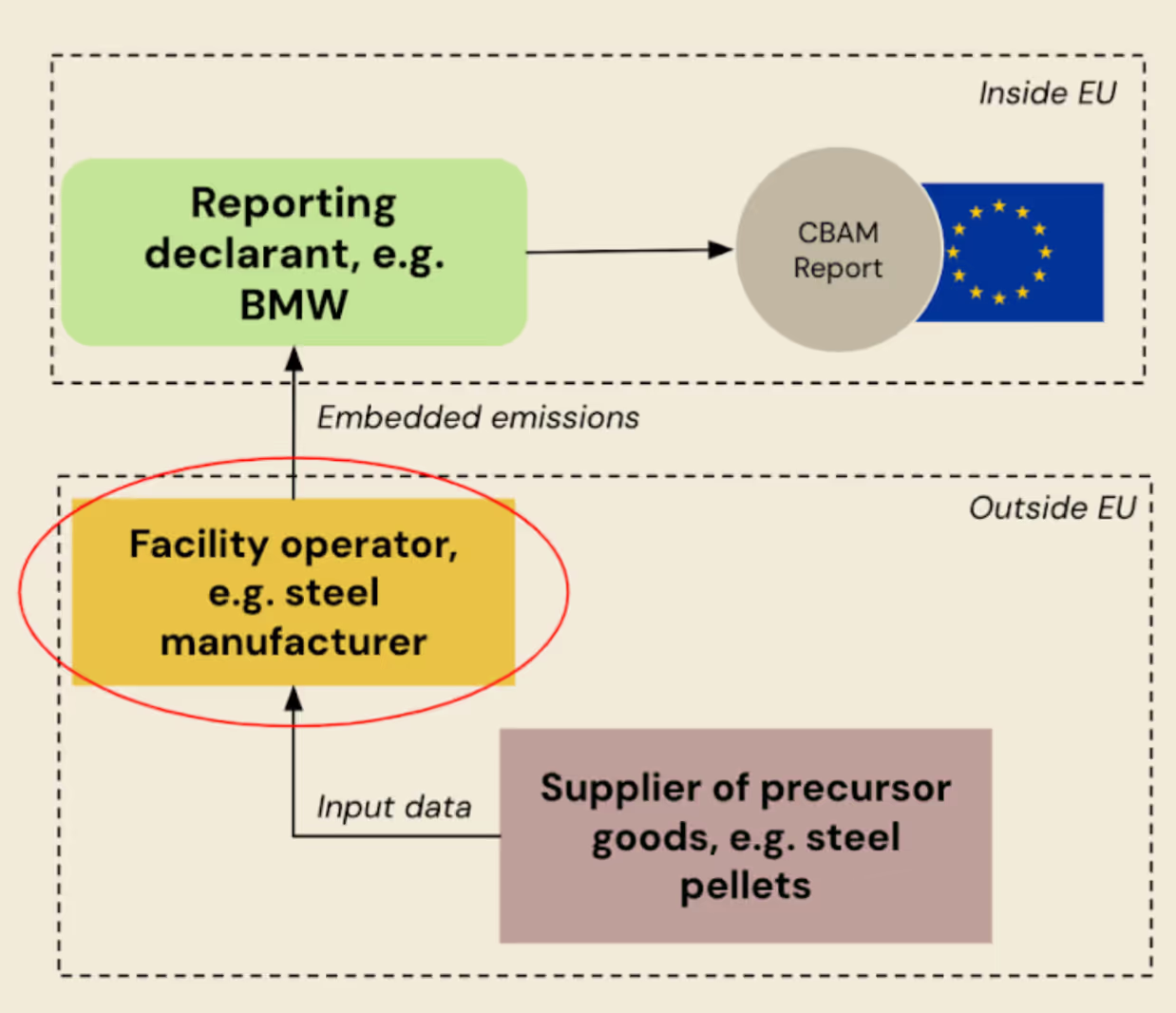

Who is involved in CBAM?

CBAM involves multiple stakeholders with specific responsibilities:

Credit: Plan A

CBAM and supply chains

As seen above, CBAM is a supply chain-focused policy requiring EU importers to engage with their suppliers outside the EU to collect embedded emissions data. This has significant supply chain implications, requiring companies to map their value chains, assess suppliers’ emissions data, and ensure compliance with reporting obligations.

CBAM incentivises decarbonisation, as lower-emission products can avoid higher certificate costs, potentially reshaping trade patterns and supplier relationships. Companies should use this opportunity to rethink supplier engagement, improve data collection, and align sustainability strategies to maintain market access and competitiveness in a low-carbon economy.

Expected economic and environmental impacts of CBAM

The economic impact of CBAM is still being assessed as it rolls out. In 2021, the European Commission estimated that CBAM could bring in around €5–14 billion per year, depending on carbon price levels and scope.

Regarding environmental impacts, CBAM is expected to cover approximately 50% of EU imports' emissions by 2026. For example, in 2022, the EU imported 1.2 billion tonnes of CO2 from non-EU countries.

Insights from the first year of CBAM

Credit: Unsplash

As CBAM enters its second year of implementation, it is worth reflecting on what has happened over the past year in this regulation. Around 20,000 CBAM reports were submitted per quarter since October 2023, with around 10,000 repetitive declarants in the first 12 months.

Most declarants come from Germany, Italy, and Poland, with the top countries of origin in quantity supplied from Ukraine, Russia, and Türkiye. Regarding the number of imports, China is the number 1 country of origin. Regarding sectors, the most imports of CBAM subject goods were iron and steel with 69%, fertilisers with 17%, cement with 9% and aluminium with 5%.

International response

Since CBAM's announcement in 2022, several countries have begun developing their carbon adjustment mechanisms. The UK, for instance, plans to implement a system by 2027, and others are considering setting up carbon pricing mechanisms, such as Türkiye and Brazil.

As a hybrid climate and trade policy, CBAM has faced criticism from various EU trade partners. Many argue it favours carbon pricing over alternative decarbonisation approaches and disproportionately affects producers in developing countries with carbon-intensive processes. Nations like China and India have labelled CBAM protectionists and threatened World Trade Organization (WTO) complaints, citing discriminatory effects and the gradual phase-out of free EU emission allowances. Despite these objections, the EU insists CBAM complies with WTO rules.

Trade flows have not yet been impacted, and business continues as usual, as producers of CBAM goods are absorbing CBAM implementation costs (related to carbon accounting and reporting requirements) and continuing to trade with Europe. However, as carbon prices are due to be paid, this will likely change as predicted by the EU (see above economic impacts).

Industry response

Although paying the carbon price under CBAM won't take effect until 2026, EU importers and their suppliers already feel its administrative impact.

Importers must meet reporting requirements and familiarise themselves with the new carbon accounting rules. It remains uncertain whether this added administrative burden alone will prompt some importers to cease sourcing certain goods from outside the EU.

Meanwhile, in the EU, the European Steel Association called for the timely implementation of CBAM in a January 2025 statement. They proposed key changes, such as replacing the 'de minimis rule' with a weight-based threshold and including steel-intensive downstream goods to protect competitiveness.

Important developments to follow

- New EU portal for operators of third-country installations

Starting January 1, 2025, a new portal section of the CBAM Registry is live to enable installation operators outside the EU (suppliers) to upload and securely share their installation and emissions data with EU reporting declarants in a streamlined manner. Key benefits of this free tool include centralised data uploads, confidential handling of sensitive business information, and automated CBAM report population for EU declarants.

The portal is live and can be accessed here, but an EU login is required. To support a smooth onboarding experience, a series of comprehensive video tutorials, “CBAM Registry Access for Non-EU Installation Operators”, has been published here. We encourage you to review these resources and start utilising the portal today.

- Several ongoing studies

The EU has opened several studies to assess the various elements of CBAM in the transitional period. The studies include:

- Study on carbon price paid in third countries

- Study on default values

- Study on electricity as CBAM good

- Study on indirect emissions

- Study on monitoring/reporting, verification/accreditation and free allocation

- Study on potential CBAM scope extension to downstream goods

- Study on potential CBAM scope extension to other sectors and transport of CBAM goods

- Study on economic impacts of CBAM

These investigations, conducted by several working groups commissioned by the EU, combined with a November 2024 meeting of the CBAM Expert Group discussing ideas for simplifying the CBAM, suggest that changes to some aspects of the CBAM can be expected before the definitive period starts in 2026.

Share your CBAM reporting experience

The first year of CBAM highlights its complexity and potential to reshape global trade and environmental policy. While economic impacts still unfold, administrative requirements have influenced supply chains and companies worldwide. Ongoing studies and feedback will shape CBAM’s future form, likely balancing climate objectives with economic and trade considerations.

Let us know your experience with CBAM at [email protected]. Plan A actively provides feedback on EU consultations at national and international levels. With your permission, we will leverage this feedback to enhance your voice in actively helping the EU set proportionate regulations that promote environmentally friendly business decisions and growth.

.avif)