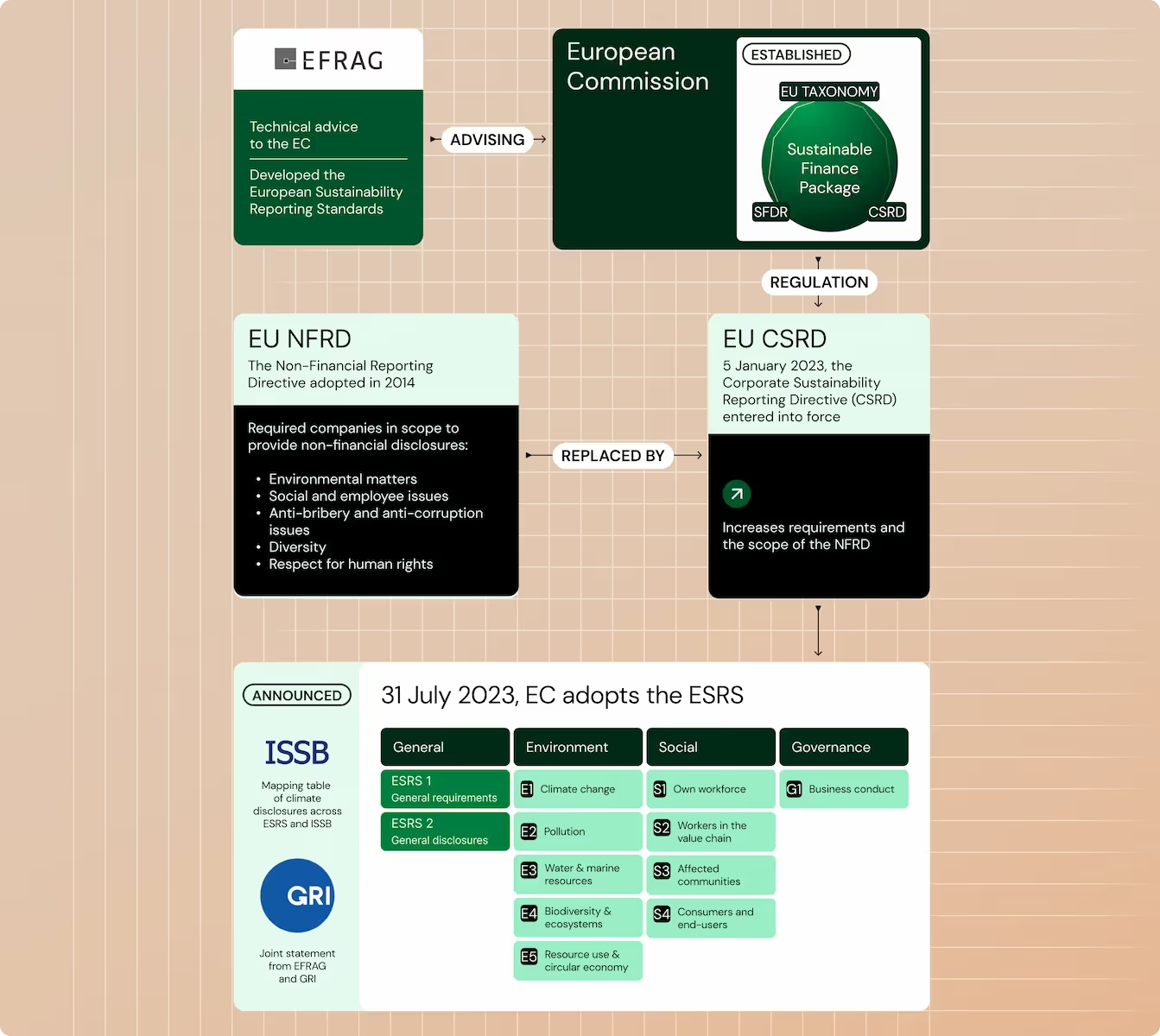

The Corporate Sustainability Reporting Directive (CSRD) mandates comprehensive ESG reporting regulations within the EU and, in some cases, beyond its borders, enhancing the previous Non-Financial Reporting Directive (NFRD). It introduces more detailed reporting standards and broadens the scope to include a wider range of companies, including listed SMEs and non-EU companies with significant EU activities. This directive aims to improve transparency and comparability of sustainability information, ensuring businesses provide accurate and reliable data on their environmental, social, and governance (ESG) performance.

Source: NOSSADATA

What is the timeline of CSRD for companies’ reporting?

The Corporate Sustainability Reporting Directive (CSRD) sets specific timelines for companies to comply with the sustainability reporting requirements based on size and classification. Here's the detailed timeline:

1. Large companies and parent companies of large groups (with over 500 employees)

- Financial years starting on or after 1 January 2024: These companies, subject to the previous NFRD, are transitioning to CSRD compliance.

- Reporting under CSRD: These entities must include their first CSRD-compliant sustainability report in 2025, covering the 2024 financial year.

2. Large companies meeting two out of three criteria: over 250 employees, €50 million in turnover, €25 million in total assets

- Financial years starting on or after 1 January 2025: These companies will begin reporting under CSRD.

- Reporting under CSRD: The first report will be due in 2026, covering the 2025 financial year.

3. Listed small and medium-sized enterprises (SMEs), small and non-complex credit institutions, and captive insurance undertakings

- Financial years starting on or after 1 January 2026: These entities will begin their CSRD reporting.

- Reporting under CSRD: Their first report will be due in 2027, covering the 2026 financial year.

4. Non-EU companies with substantial activity in the EU (net turnover of more than €150 million in the EU and at least one subsidiary or branch in the EU exceeding certain thresholds)

- Financial years starting on or after 1 January 2028: These companies must comply with CSRD requirements.

- Reporting under CSRD: The first report will be due in 2029, covering the 2028 financial year.

Additional points

- Phase-in requirements: Companies meeting the criteria for the first time will benefit from phased-in disclosure requirements, as outlined in ESRS 1, Appendix C.

The CSRD timeline is done through a phased approach, ensuring a smoother transition and giving companies enough time to prepare for the more extensive reporting requirements. Companies in the scope of the CSRD shall start collecting relevant data now.

Deepen your knowledge of CSRD with our resources

Here are some resources to progress towards CSRD readiness:

- Learn how to prepare for the CSRD

- Access a detailed guide on the ESRS

- Discover the critical steps of the ESG reporting process

If you need dedicated support to prepare your business, schedule a call today to speak with Plan A’s team.