Les critères environnementaux, sociaux et de gouvernance (ESG) et leur influence exponentielle sur les entreprises prenant des mesures climatiques, amenant celles-ci à placer de plus en plus la « durabilité » au cœur de leur stratégie d'entreprise, ont finalement conduit de nombreuses entreprises à être incertaines quant à la meilleure manière d'allouer leurs ressources pour une transition durable.

La durabilité peut être un sujet accablant et les approches pour prendre des mesures climatiques en entreprise sont nombreuses ; ainsi, si une entreprise tente de développer une stratégie globale sans aucune orientation, elle risque de gaspiller de manière significative ses ressources. Bien que cela puisse sembler paradoxal, les entreprises favorisent de plus en plus l'influence des réglementations car elles agissent comme des lignes directrices pour les bonnes pratiques - notamment en matière de climat.

À la lumière du prochain cycle de reporting et de la prise de conscience croissante de la valeur à long terme de l'intégration de la durabilité en tant que composante clé de la stratégie d'entreprise, il est d'autant plus important que les entreprises comprennent et tiennent compte de l'influence des différents organismes de réglementation et cadres réglementaires.

En conséquence, cet article présentera plusieurs organismes de réglementation, réglementations et cadres réglementaires clés en matière d'ESG qui affectent les entreprises de toutes tailles et formes. De plus, cet article détaillera l'influence des organismes de réglementation sur les pratiques commerciales durables ; et enfin, comment les entreprises peuvent utiliser les réglementations et cadres réglementaires de l'ESG à leur avantage.

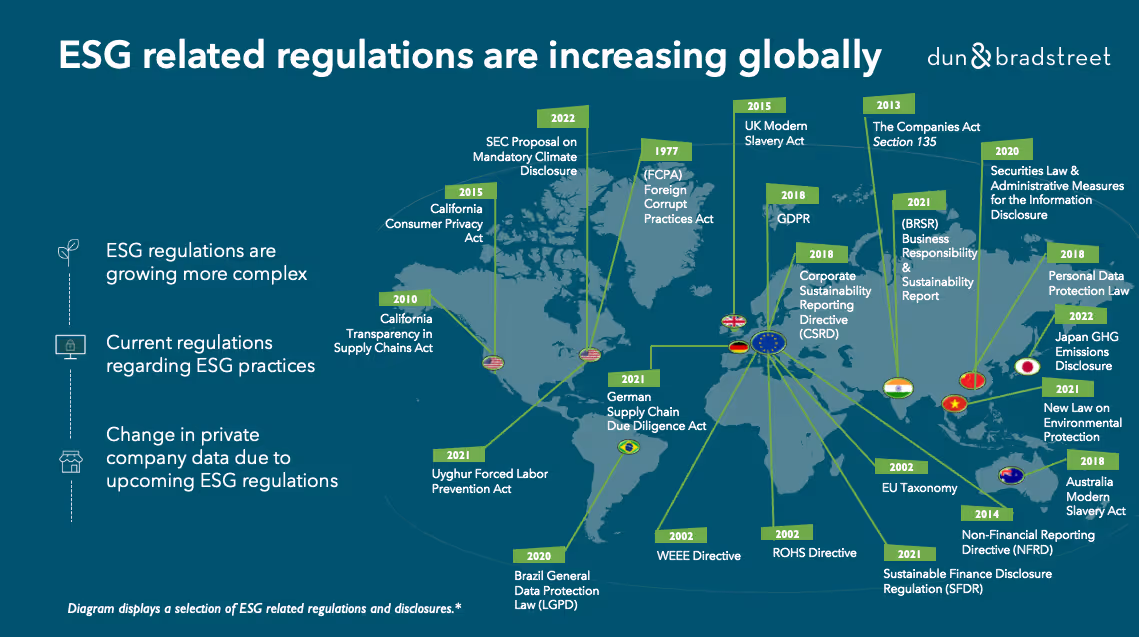

Le paysage actuel des réglementations et des cadres ESG

Certaines des principales régulations et cadres de référence qui sont d'une importance vitale pour les organisations incluent :

Groupe de travail sur les divulgations financières liées au climat (TCFD).

La Task Force on Climate-Related Financial Disclosures (TCFD) a été créée en 2015 par le Financial Stability Board (FSB) international pour développer des divulgations cohérentes des risques financiers liés au climat à l'usage des entreprises, des banques et des investisseurs. L'objectif est d'assurer la stabilité financière au niveau mondial, car le changement climatique aura un impact négatif sur notre économie. Le principal objectif du reporting TCFD est de divulguer les risques et opportunités liés au climat d'une entreprise, ainsi que l'impact financier que ceux-ci pourraient avoir sur les opérations et le modèle économique de l'entreprise.

Corporate Sustainability Reporting Directive (CSRD)

La Directive sur la publication d'informations en matière de durabilité des entreprises (CSRD) est la nouvelle législation de l'UE qui exige que toutes les grandes entreprises publient régulièrement des rapports sur leurs activités environnementales et sociales. Elle aide les investisseurs, les consommateurs, les décideurs politiques et d'autres parties prenantes à évaluer la performance non financière des grandes entreprises. Ainsi, elle encourage ces entreprises à développer des approches plus responsables en matière d'activité commerciale. Par exemple, elle modifie radicalement le champ et le type de reporting en matière de durabilité des entreprises. Avec la CSRD, la Commission européenne définit pour la première fois un cadre de reporting commun pour les données non financières.

Non-Financial Reporting Directive (NFRD)

La Directive sur la publication d'informations non financières (NFRD) exige que les entreprises concernées publient un rapport non financier sur leur performance ESG en même temps que leur rapport de gestion annuel. La NFRD vise à aider les investisseurs, les organisations de la société civile, les consommateurs, les décideurs politiques et autres parties prenantes à évaluer la performance non financière des grandes entreprises et encourage ces dernières à adopter une approche responsable des affaires.

UK Disclosure Framework for Net Zero Transition Plans

Le Cadre de divulgation du Royaume-Uni pour les plans de transition vers le net zéro est un ensemble de lignes directrices que les entreprises peuvent utiliser pour rendre compte de leurs efforts de transition vers des émissions nettes nulles et soutenir la transition vers une économie à faible émission de carbone. Le cadre a été élaboré par le Groupe de travail sur la divulgation des informations financières liées au climat (TCFD), une organisation créée par le Conseil de stabilité financière (FSB) pour promouvoir une divulgation cohérente et transparente des risques et des opportunités liés au climat, alors que les entreprises annoncent de plus en plus des engagements de neutralité carbone sans publier de plans pour soutenir leurs objectifs. Il fait partie de l'engagement du gouvernement britannique à devenir le "premier centre financier aligné sur le net zéro au monde.

Le 8 novembre 2022, le groupe de travail sur le plan de transition du Royaume-Uni (TPT) a publié son Cadre de divulgation et guide de mise en œuvre. Il s'appuie sur des normes et recommandations existantes et émergentes, notamment le TCFD, l'Alliance financière de Glasgow pour le net zéro (GFANZ) et le Conseil des normes de durabilité internationales (ISSB).

CDP - Un cadre de publication d’informations sur le climat pour les PME

CDP est un cadre de déclaration volontaire populaire que les entreprises utilisent pour divulguer des informations environnementales à leurs parties prenantes (investisseurs, employés et clients). Le système de réponse en ligne est maintenant ouvert, et le mercredi 26 juillet 2023 est la date limite pour les entreprises qui souhaitent recevoir un score CDP.

Les plans de l'UE en matière de finance durable

Dans le contexte des politiques de l'UE, la finance durable est comprise comme étant une finance visant à soutenir la croissance économique tout en réduisant les pressions sur l'environnement et en tenant compte des aspects sociaux et de gouvernance.

EU’s “Fit for 55”

Le paquet Fit for 55 de l'Union européenne vise à réduire les émissions de gaz à effet de serre de 55 % d'ici 2030. La Commission européenne a proposé ce paquet en juillet 2021 ; et en avril 2023, le Parlement européen a confirmé les objectifs climatiques révolutionnaires. La législation comprend une refonte du système d'échange de quotas d'émission (SEQE), la création d'un marché parallèle du carbone et un fonds social climatique de 86,7 milliards d'euros. Cette législation innovante marque un tournant mondial vers des politiques plus respectueuses de l'environnement et garantit un avenir plus durable pour l'UE et le monde.

L'influence des réglementations ESG sur la durabilité des pratiques commerciales

Le risque climatique est un risque financier.

La croissance continue des normes de reporting à l'échelle mondiale souligne davantage une telle affirmation, et cela n'est pas surprenant ; ces normes sont essentielles pour garantir une évaluation harmonisée du coût du changement climatique pour les entreprises et les gouvernements.

- Les entreprises qui n'analysent pas continuellement le paysage réglementaire risquent donc de s'engager dans des actions commerciales et des pratiques de reporting qui ne sont pas conformes aux politiques pertinentes.

- Il est donc essentiel que les entreprises comprennent les réglementations pertinentes qui s'appliquent à elles, les actions qu'elles doivent entreprendre pour respecter ces réglementations, et les futures réglementations qui pourraient les influencer.

- Les entreprises devraient rechercher des cadres volontaires pour s'assurer qu'elles établissent des rapports percutants et efficaces, réduisant ainsi les risques financiers et augmentant la transparence parmi les parties prenantes.

- Les entreprises qui sont proactives auront l'opportunité de devenir des pionnières dans la transition vers une économie durable.

Comment les entreprises peuvent-elles utiliser les réglementations et les cadres ESG pour mettre en œuvre stratégiquement des actions climatiques ?

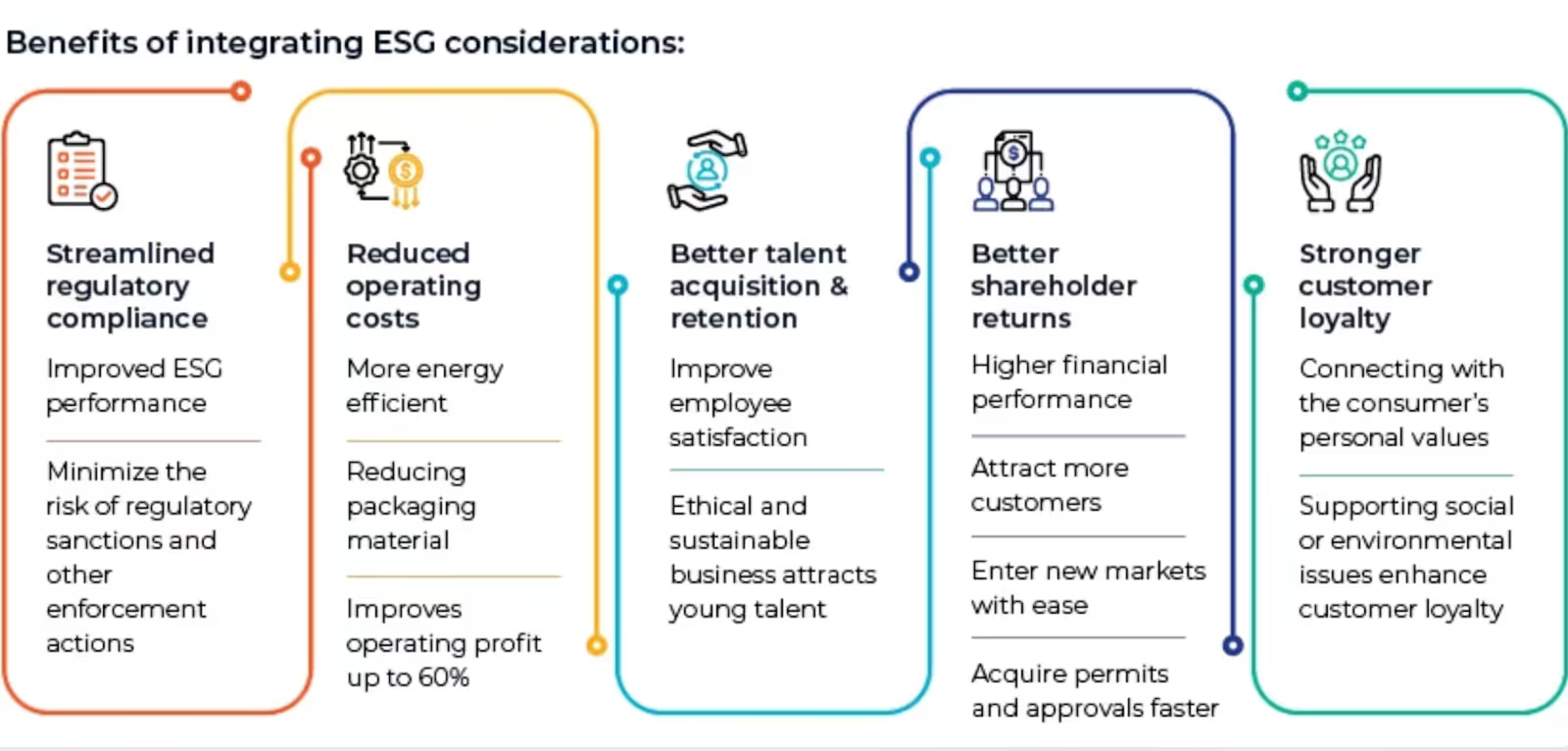

L'application des normes réglementaires agit comme un guide pour la pratique commerciale, influençant l'action climatique des entreprises et guidant la pratique durable. Simultanément, la mise à disposition de cadres volontaires que les entreprises peuvent utiliser comme guide dans des domaines clés - tels que le reporting - n'est pas moins importante dans la transition vers une économie plus durable.

La mise en œuvre de tels objectifs et cadres de neutralité climatique s'est révélée très efficace. En unifiant davantage la manière dont les entreprises et les pays comprennent les concepts liés au changement climatique, à la durabilité et à la décarbonation, de tels cadres facilitent l'alignement entre le discours et l'action. Cependant, il convient de noter que la majorité de ces cadres se concentrent sur l'évaluation historique, et avec une planète qui se réchauffe davantage, rendre compte du passé ne nous aidera pas à nous préparer à l'avenir.

Les entreprises peuvent tirer parti des réglementations et des cadres mentionnés ci-dessus de différentes manières, notamment :

- Garantir de manière proactive la conformité à la Directive sur la communication d'informations en matière de durabilité des entreprises (CSRD) grâce à une surveillance active et à des mesures de reporting (par exemple, la collecte de données) afin d'éviter des sanctions importantes.

- Pour les organisations faisant rapport sur le NFRD, comprendre que le premier rapport CSRD des entreprises dans le champ d'application du NFRD est attendu en 2025 pour l'année financière 2024. Étant donné que ce n'est qu'une question de temps avant que le NFRD ne soit remplacé par la CSRD, les entreprises doivent chercher à s'informer sur la CSRD et sur son impact sur leur entreprise.

- Pour les entreprises concernées par le TCFD, il est essentiel de comprendre que les sociétés ayant une année financière calendaire devront inclure pour la première fois les obligations de divulgation financière liées au climat dans leur rapport annuel et rendre compte de l'exercice financier débutant le 1er janvier et se terminant le 31 décembre 2023. Cela revêt une importance fondamentale pour garantir que la durabilité soit une priorité stratégique tout en atténuant les risques financiers supplémentaires.

- Les organisations devraient volontairement utiliser le Cadre de divulgation du Royaume-Uni pour la transition vers la neutralité carbone afin de bénéficier d'une manière cohérente et transparente de rendre compte de leurs efforts climatiques, tout en accélérant activement la transition vers la neutralité carbone et en soutenant la transition vers une économie à faible émission de carbone. Le cadre fournit également aux investisseurs, aux clients et aux autres parties prenantes les informations nécessaires pour comprendre les efforts d'une entreprise vis-à-vis des risques et des opportunités liés au climat. En tant que tel, le cadre de divulgation du Royaume-Uni offre une valeur immense à ceux qui cherchent à exploiter stratégiquement la durabilité tout en contribuant activement au processus global de décarbonation.

- Les entreprises peuvent utiliser le cadre du CDP pour mieux comprendre et rendre compte des indicateurs critiques liés au climat sur lesquels les PME devraient rendre compte et utiliser pour informer leurs divulgations. Inclure ces informations dans leurs rapports principaux ou lors de l'utilisation d'autres plateformes de collecte ou de reporting de données permettra à ces entreprises de répondre aux demandes de transparence des parties prenantes ; de cartographier et de comprendre les risques au sein de leur chaîne d'approvisionnement ; et de mesurer leurs performances dans la transition vers la neutralité climatique, ce qui leur permettra ainsi de bénéficier d'un avantage concurrentiel.

- Enfin, rendre compte des risques climatiques et de la durabilité en comprenant et en garantissant le respect de diverses lois, telles que la Loi climatique de l'UE, l'UE Fit for 55, le Plan de finance durable de l'UE et la Loi allemande sur la protection du climat.

En fin de compte, la durabilité doit devenir la norme mondiale au sein des chaînes d'approvisionnement des entreprises mondialisées afin d'atteindre des objectifs climatiques à long terme essentiels, tels que les Objectifs de développement durable des Nations Unies. À cet égard, les organismes de réglementation et les cadres sont absolument essentiels pour minimiser les coûts financiers et environnementaux auxquels sont confrontés les gouvernements, les entreprises et la société dans son ensemble.

De telles réglementations fournissent des directives claires pour des pratiques durables, garantissant ainsi que les entreprises sont informées des exigences qu'elles doivent respecter pour éviter des sanctions, des actions qu'elles doivent entreprendre pour intégrer des pratiques durables, et donc comment les entreprises peuvent allouer leurs ressources pour contribuer positivement au parcours global vers la décarbonation.

En conséquence, la poursuite de la réglementation ESG signifie que les entreprises doivent prendre des mesures immédiates pour s'assurer qu'elles surveillent et rendent compte avec précision de leurs performances non financières, tout en entreprenant également des actions concrètes vers la décarbonation.

Protégez l'avenir devotre entreprise en vous alignant sur les réglementations ESG . Prenez rendez-vous avec Plan A dès aujourd'hui.